FREE NEWSLETTER

MY WIFE AND I have around $50,000 of emergency funds (~8 months of expenses). Considering that the job market is shaky, we feel comfortable holding this much cash.

Of course, it’s important to make the most out of your savings, so I want to share some options available to earn ~4% yield on your money.

Keep in mind that you should only use the following options for emergency savings and specific saving goals (e.g. a downpayment for a house).

Here are some options available to you depending on your goals, tax situation, and desired yield:

A savings account is a decent option to store your emergency funds/savings. Savings accounts are FDIC insured up to $250,000 (some might offer even more), so your money is generally protected.

You should typically evaluate savings accounts based on:

Currently, some of the banks that pay 4%+ are no-name banks that you’ve never heard of. Some of them are part of the bigger banks, but have no in-office branches.

Here are some options that you’ve may have heard of and their yields:

If you do want to open a HYSA, take some time to research these banks using the criteria above. I personally used CIT Bank for my savings some time ago, but switched because of their poor user interface and login issues.

The main benefit of using a HYSA is the FDIC insurance, which might not be applicable to other options discussed further:

2. Money Market Fund

Big brokerages like Vanguard or Fidelity offer Money Market Funds (MMFs).

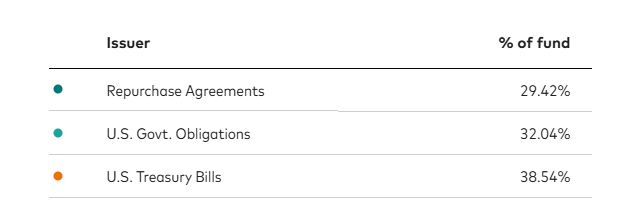

Money Market Funds are mutual funds that try to maintain a stable share price of $1. These funds invest their assets in cash, U.S. government securities, and/or repurchase agreements.

For example, Vanguard has 2 main ones:

VMFXX (Vanguard Federal Money Market Fund) with a 3.89% yield. The portfolio composition is:

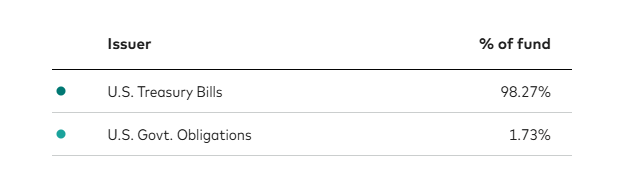

VUSXX ( 3.88% yield with composition:

VUSXX is generally a better option as of now because it has an identical yield, but more of the income will be exempt from state and local taxes since it holds T-bills.

Keep in mind these two funds are not FDIC insured. They are SIPC insured, so if anything happens to Vanguard or Fidelity, your money may be protected.

However, it’s possible that the share price can go below $1. In 2008 and 2020, the Federal Reserve stepped in and provided liquidity options to prevent that from happening.

It will take you about T+2 days to withdraw money from this fund. Both funds have over $100 billion in assets.

I personally use VUSXX for my savings. However, if you are in a 37% marginal tax rate, you may also consider a Municipal Money Market Fund. Because it’s not taxable on a federal level (and in some instances on the state level too), people who are in a high marginal tax rates might get a bigger after-tax yield by holding them.

3. T-Bills

Treasury bills (T-bills) are short-term debt instruments issued and backed by the U.S. Treasury. Treasury bills are issued for terms of 4, 8, 13, 17, 26, and 52 weeks.

T-bills can be purchased from banks, brokers (like Fidelity), and directly from the Treasury through Treasury Direct (this website is absolutely terrible to navigate!)

Current yields:

T-bills are exempt from state and local taxes. These are as safe as savings accounts as they are backed by the Treasury. The only problem is that your money is locked in for that length, unless you sell early in a secondary markets.

If you don’t want to buy Treasury bills directly from Treasury Direct or other brokers, there are ETFs (e.g VBIL 3.86% yield) that only hold T-bills. However, they have expense ratios, so your yield typically will be lower than buying directly.

Overall, I personally suggest Money Market Funds or HYSAs. They are the easiest to understand and work with, but you have to decide which product makes the most sense for you.

Just don’t use banks that pay 0.01% interest!

Which option do you currently use? Let me know!

![]() Bogdan Sheremeta is a licensed CPA based in Illinois with experience at Deloitte and a Fortune 200 multinational.

Bogdan Sheremeta is a licensed CPA based in Illinois with experience at Deloitte and a Fortune 200 multinational.

Schwab money market fund

No Penalty CD Ladder. Currently earning 4.3% APY.

JAAA, ST bond clo ETF is my go to. 5.5%. Very stable AAA rated CLO’s .

Translation, please?

Janus Henderson Investors

JAAA AAA CLO ETF.Provides exposure to the high-quality, floating rate CLO market in a liquid, transparent manner.

Diversifying Fixed Income AAA-Rated Collateralized Loan

Obligation Exposure.

YTD Return 4.79 as of 12/9/2025

Info from Janus Henderson website; I don’t own it or had ever heard of it before seeing the comment here.

I expect the “Translation, please?” comment reflects Jonathan’s strong editorial guideline against just using stock symbols in articles, preferring we spell out company or fund names instead. I find myself thinking of his gentle nudge when I self edit a post or reply.

Thanks, Chris. And Bill, you hit the nail on the head: https://humbledollar.com/forum/rules-of-the-road-by-jonathan-clements/

I recently read an article by an author suggesting that our cash cushion should be more on the order of 4 years – a period that should be sufficient in most circumstances to avoid selling into a falling market to meet our cash needs. I think that is a little extreme, but in our current economic climate, keeping 2+ years of cash and equivalents in our IRA’s to meet our annual RMD needs doesn’t seem all that crazy.

The question you raise as to how and where to invest any such funds in absolutely relevant as the available options are many and care needs to be taken with offers that promise outsized returns. Personally, I keep a fair amount of cash in the treasury backed MMF in my brokerage account. All of the suggestions you noted are equally good, and all will be substantially better than the de minimis returns that bank checking and savings accounts continue to offer.

I use Schwab’s Money Market fund SWVXX. It’s currently yielding about 3.8%. I previously used a High Yield Savings account at CIT Bank, the online branch of First Citizens Bank. Several years ago I was the victim of a wire transfer fraud at CIT Bank involving bogus two factor authentication approvals. I was very dissatisfied with their response. Only after 7 weeks of badgering them and letter writing to various govenment agencies did they agree to refund my money. It was a very disturbing response from a top 20 bank. Now I use Schwab for their safety protocol and my desire to simplify my personal accounts. I would say beware of no name banks and make sure you understand the rules about what financial institutions you allow to interact with your primary brokerage. Read the fine print.

We have a cash allocation in a 401(k) stable value fund. This is far larger than just a short-term emergency fund or specific savings goals. Bogdan, your caution to limit cash to that amount may be fine for you at your life stage, but at mine, I prefer much more.

For more accessible cash, we use Fidelity Premium Money Market (FZDXX). It has a $100,000 minimum to open, but no ongoing minimum balance requirement.

Other online banks to look at:

Ally

CapitalOne 360 premium savings

American Express

VMLUX – 75%

VANGUARD LTD TERM TAX EXEMPT ADMIRAL CL

7012 Bonds with an Average duration 2.6 years

30days SEC yield as of 12/04/2025 3.05% A

VBIL – 25%

VANGUARD 0-3 MONTH TREASURY BILL ETF

26 Bonds with an Average duration 0.1 years

30days SEC yield as of 12/04/2025 3.86% A

I admit I never really understood the concept of holding onto cash for emergencies or other short-term needs. I always thought it was better to have access to lines of credit with a HELOC or Morgan Stanley, pledging part of my portfolio as collateral. I reasoned that holding onto liquid assets never seemed to yield as much as other long-term instruments.

Please tell me if I’ve been doing all wrong for the past 50 years and why. It seemed to be a less expensive way to handle the unexpected. Thanks.

I recall a number of banks closing down HELOCs in 2008 during the financial crisis. I was relieved to have some cash on hand when the bank pulled mine. Personally, I’ve never lost sleep over the opportunity cost of cash but I won’t forget that unpleasant surprise from the bank.

If you’ve been doing it for 50 years, I’m sure there’s no argument that would persuade you that your way was not the best way. I know that when I used a HELOC just to get me through three property transactions occurring within days of each other, I hated paying the interest that accrued. Maybe I didn’t know how good I had it! No doubt your preferred strategy has been a good choice with equities on a roll, as recently. For me, relying on HELOCs and the like for major funds through a rough patch would definitely interfere with my sleep.

Times change, so what I felt worked for me in the past does not mean it’s a good strategy going forward.

We are moving into a new CCRC early next year. This eliminates most of my causes for emergency cash.

At this point, any financial disasters will affect my heirs. We are pleasantly coasting, ready for what comes next.

I was more curious than anything else. Thanks for your comments.

Got it. Glad it worked out for you. I was too busy with professional life to afford the time and attention I feel would be needed to do what you did, but see how it could be advantageous, given a cooperative market. Concern about the latter led me to focus on maximizing my retirement accounts and using cash as best I could. Best wishes for your upcoming CCRC move!

SPAXX at Fidelity or SMB for tax free monthly income.

If you have 100k+ of cash at Fidelity, FZDXX pays 16 basis points more than SPAXX, but still 12 points below VMFXX.

FZDXX minimum is $10k in an IRA.

I keep extra cash in my coinbase account. USDC = 4%

Thanks for this. We keep way too much in a virtually no interest account. I justify it as being convenient, but I’ll be checking out some of the options you mention.

I use high yield online savings accounts. When selecting one of these banks, make sure that it is a bank and not an online pass-thru entity that takes your money and passes it on to a real bank. Rare, but there have been issues when there was mismanagement between the online sudo-bank and the real bank. Sites to verify banking: https://banks.data.fdic.gov/bankfind-suite/bankfindhttps://

mapping.ncua.gov/ResearchCreditUnion

We have Fidelity and Vanguard brokerage accounts. We use Fidelity’s billpay to pay our bills. Each offer checking accounts and EFT capability. Not sure of any delay getting money out. Since May 28, 2024, the standard settlement cycle for most securities, including mutual funds like VUSXX, has been T+1 (one business day after the trade date), not T+2. Prior to this change, the standard was T+2.

When bond funds started losing money some years ago, we switched into money markets. Now all the fixed portion of our asset allocation is in the money market core account at Vanguard. If rates go lower in MMs then we may shift back into intermediate bond ETFs

Yep, no bonds for me, I am 85% S&P and 15% CASH. My cash is in Marcus account which is a part of Goldman Sachs. Current rate is 3.65%. My market cash is in Vanguard VMFXX and Fidelity FDRXX. This works for me.

I’m both a minimalist and a cheapskate so here’s where I’ve ended up: Fidelity as our primary brokerage AND bank, Schwab as a back-up. Why? Fidelity is the only one of the three major brokerages that has a lockdown feature to prevent fraudulent ACATS transfers, plus (unlike Schwab) they pay competitive (with high-yield savings accounts) interest on sweep funds in money market accounts. They also offer a Visa credit card whose cash-back feature nets us several hundred dollars a year since we charge everything we can on it and pay it off monthly, along with a debit card that reimburses transaction fees worldwide. Good luck finding a bank that offers these benefits.

Given the omnipresent threat of cyber attacks temporarily impeding account access I think it’s prudent to have at least one backup brokerage. Schwab fulfills that role for us nicely. By intention and design their yields on both bank savings and checking accounts and sweep money market accounts on the brokerage side are pitiful, so we keep a bare minimum in savings and checking there (which gives us a second debit card to use which like Fido’s reimburses us for ATM fees worldwide) and remaining cash in SGOV.

Finally, on the investing side, we hold almost exclusively Vanguard ETFs at both brokerages, thereby taking advantage of the one thing Vanguard does well (running low-cost funds) while sidestepping their lousy customer service, primitive website and tools and so-so security. IMHO two great brokerages make regular banks and credit unions superfluous.

Kevin, I concur with your use of Fido; similar to my own profile and use of their services. I have Schwab as a backup but have a very small acct presence there.

Kevin,

Excellent Comment!!

We have the same sort of setup, but with different companies.

Additionally, because I am very conservative about our personal funds PLUS I worked in the IT field for over 4 decades, I have a “bug” … ahem … about ‘cybersecurity’. So we keep about 1 month’s food expenses in cash.

An excellent bank that reimburses debit card fees worldwide is USAA bank. Their security is excellent, but interest is paltry.

I survived a few incidences with brokerage outages, credit card freeze, ATM glitches. Therefore my recommendation is to have 2 different brokerages, 2 credit cards from different issuers, and 2 different bank accounts.

I depend on banks for Zelle payments, cash access with wide ATM network, secured and fast wire transfers for large transaction, IRS estimated tax payment, safe deposit box, notary services, on top of FDIC insurance and instant remote check deposit from home. No brokerage offers these services. My mom-and-pop ethnic grocery stores, restaurants, hair services prefer cash to save on VISA fees.

Quan, the characteristics you laid out in your “bank requirements” can be fulfilled with Fidelity’s Cash mgt account with the exception of safe deposit box & notary services(maybe). With Fidelity’s CMA you can have your cash swept into FDIC partner banks on a nightly basis thus exceeding the $250k bank acct limitation up to a max of $5m($250*20 banks).

https://www.fidelity.com/spend-save/fidelity-cash-management-account/overview

Year 1-2 cash–Vanguard MM, 3.78% and falling

Year 2 cash–Fixed annuity 5.25%, fixed for 2 yrs

Year 3 cash–Fixed annuity 6.0%, fixed for 3 yrs

Year 1 has 100% liquidity

Year 2 has terrible liquidity (maybe 10%/yr), backed up to 250k by state

Year 3 has terrible liquidity (maybe 10%/yr) backed up to 250k by state

Instead of chasing yield on my cash I chase simplicity. Since my taxable account is on the Schwab platform I just keep it in their money market and couldn’t care less what the rate is. Am I losing a few dollars by not seeking out the highest yield absolutely do I have peace of mind knowing exactly where my cash is and I can simply transfer it to my checking account , yep.

You are on the spot I think Lester. I was worried about ROI in my accumulation phase of wealth. Now, I find not thinking about that so freeing. But recently, I did open a MM account that my credit union offered. It gives 3.25% but, compounded daily.

So, hey, switching money to my checking in the same CR is simple and I have $2k a month automatically moved to it so it grows enough for me.

SWVXX

I have two HYSA, one with Amex (opened it for the points) and one with Ally (like the “buckets” you can allot savings to, good visual). Current yields around 3.3%. Have been up as high as 4.25%.

We have more cash than a proper “emergency fund” should because we may make a down payment on a second property within the next year or two. But it’s still under FDIC limits.

My husband works for an accounting firm and has asked me to stay away from money markets while he’s still working because they complicate his regular independence audits. Once he retires, we’ll revisit that.

I have gotten into the habit of purchasing T bills via Schwab on a laddered basis for my cash reserves if need be, I can sell them before maturity. And the yields range from 3 1/2 to 4 1/2%.

A while ago, as we formulated our post-retirement plan, I read that bear markets average 2 to 3 years. So we took the 3-year view and created a bucket for each:

Year 1 Cash: This is our local checking (1/3)(lousy interest) and our Fidelity Bill Pay (2/3)(SPAXX). We live off of this.

Year 2: Is the one-year cash equivalent in Fidelity money markets that serve as our “sweep accounts” in various IRA’s. I never let the sum of these go below the year-2 value.

Year 3: One year equivalent held in a T-Bill ladder.

(Year 2 and 3 are adjusted for 3% inflation)

Everything else is fully invested in a 60/40 portfolio.

I use Treasury Direct and while I agree the website is not the best, once you become familiar with it, it is fine. It is easy to reinvest every month if you choose to or get the money back after it expires. I have been using it on a month-month basis for over a year now and am very happy with it.

I use Fidelity money market. Latest 7 day yield 3.61%

I have our emergency fund in Fidelity’s money market. I had been keeping a big chunk in CDs, but as the rates dropped to 4%, I moved the proceeds into the MM pot.

I keep 1-2 months in a money market fund and the next 12-18 months in ST bond funds.

For part of our emergency fund I agree with the eight reasons cited by David Enna who blogs at TIPSwatch and many other notable financial writers cited in the post to have a position in I-Bonds.

Mr. Enna has a tab titled I Bond Manifesto – Why inflation-linked savings bonds can work as part of your emergency fund if you are interested in their thinking.

Currently issued I bonds have a rate of 4.03%. This includes a fixed rate of 0.90% and the I bonds issued now will have this rate until April 30, 2026. I do not mind the clunky TreasuryDirect website.

My investment choices for cash equivalents are SGOV, Treasury Ladder, and I-Bonds