FREE NEWSLETTER

I WAS SCROLLING through social media recently and saw somebody dismiss retirement accounts as “paper wealth.” The argument was familiar: Your money is locked away and you’re waiting for permission to access it.

There’s a grain of truth here. Retirement accounts do come with rules. But much of the discussion online ignores how flexible these accounts actually are. More important, it ignores the enormous tax advantages.

Most people today will likely live well beyond age 59½. Many will spend two or three decades in retirement. Even if somebody retires early, they’ll still need assets later in life.

That’s why ignoring retirement accounts at age 30 often isn’t wise. You could end up giving away 30 or 40 years of tax-advantaged compounding.

It also isn’t an all-or-nothing decision. We can use taxable brokerage accounts, Roth IRAs and 401(k)s together. Each account serves a different purpose.

Retirement accounts also provide rebalancing flexibility that taxable accounts don’t.

Inside a Traditional or Roth IRA, investors can rebalance portfolios without triggering capital gains taxes. Somebody who wants less stock market exposure can freely sell shares and buy bonds, Treasurys or other funds without generating an immediate tax bill. That matters over long periods of time.

The other misconception is that retirement accounts are completely inaccessible until age 59½.

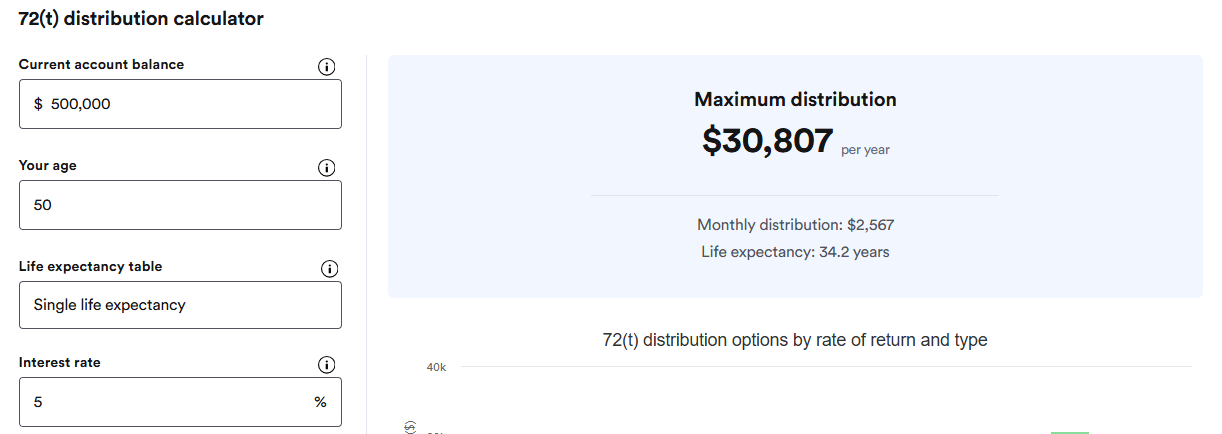

Let’s talk about Rule 72(t), also called Substantially Equal Periodic Payments, or SEPP. This IRS rule allows penalty-free withdrawals before age 59½ if specific requirements are followed.

Using online 72(t) calculators, a $500,000 retirement account could potentially generate annual withdrawals of roughly $30,000 while avoiding the normal 10% early-withdrawal penalty:

The payments must continue for a required period and the IRS rules are strict. Still, the broader point remains: There are legal ways to access retirement funds earlier than many people realize.

The Rule of 55 is another example.

If you leave your employer during or after the year you turn 55, you can often withdraw money from that employer’s 401(k) without the normal 10% penalty. Again, the money is not completely locked away until 60.

Roth IRAs may also be flexible. Contributions can be withdrawn anytime tax- and penalty-free because taxes were already paid before the money went into the account.

That doesn’t mean people should tap retirement accounts early. But accessibility is very different from impossibility.

Roth IRAs also happen to be among the most powerful wealth building tools available.

Qualified withdrawals are tax-free. Dividends compound without yearly tax bills. Investors can buy and sell investments inside the account without triggering taxable events.

You may remember a famous example about Peter Thiel. According to reporting by ProPublica, Thiel reportedly grew a Roth IRA from $2,000 to more than $5 billion between 1999 and now. He turns 59½ in 2027, meaning those withdrawals could potentially be tax-free. Imagine if he had decided to skip retirement accounts because he wanted to “live now.”

Employer matches are another point often ignored online. Skipping a 401(k) match can be one of the costliest financial mistakes people make.

Suppose an employer offers a dollar-for-dollar match on the first 3% of salary contributed to a 401(k). Before the investments even grow, that’s effectively an immediate 100% return.

Very few opportunities offer that kind of risk-adjusted benefit.

In fact, somebody could theoretically contribute, collect the employer match, later withdraw the money, pay ordinary income taxes plus the 10% penalty, and still potentially come out ahead versus investing only through a taxable brokerage account with no match.

The tax advantages extend beyond employer matches.

Inside retirement accounts:

Compare that with a taxable brokerage account, where dividends may create yearly tax bills and selling appreciated shares can trigger capital gains taxes.

Retirement accounts can also create opportunities for tax arbitrage.

Somebody contributing while in the 22% or 24% marginal federal tax bracket today might eventually withdraw money while in the 10% or 12% bracket during retirement.

State taxes can widen the advantage even more. Some states provide tax deductions on retirement contributions while later taxing retirement withdrawals lightly or not at all.

Early retirees often use Roth conversion ladders as well.

The process generally works like this:

Like Rule 72(t), there are strict rules involved. But these strategies exist because retirement accounts were never designed to be prison cells.

The larger point is that retirement planning should involve multiple tools working together. Taxable brokerage accounts provide flexibility. Roth IRAs provide tax-free growth. Traditional retirement accounts can reduce taxes during high-earning years.

None of these accounts are perfect by themselves. Together, however, they can create an extremely efficient system for building long-term wealth.

That’s why describing retirement accounts as “paper wealth” misses the bigger picture.

I don’t know who Alice Mia is, but I doubt she’s a HumbleDollarian. That was a stupid comment. She’s probably selling something.

I’m in my 40s. I’m very comfortable being a 401k and Roth IRA millionaire. I guess I’ll just have to keep “suffering” my way through life.

A good example of someone stating something against convention to bring attention to themselves. Typically works as it triggers many. Like a historian claiming at George Washington was horrific. What do they gain by saying GW was great like everyone else does? You do use this triggering claim to convey some useful info. Kudos.

Hi Bogdan, when I see the posts you referenced here on social media, I simply roll my eyes. Most of those are by insurance sales people with no real clue about financial planning. I guess you are what you read and follow…meaning those who follow that advice are destined to be broke while those who follow advice from writers like Jonathan will have a chance at a decent retirement. Appreciate the work you do here.

A lot of financial comments on social media are amusing. It was nice of you to take the time to break this one down.

I decided to pay my dues and work long and hard. I retired at 69.5 and took SS at 70.

I developed 5 retirement incomes over 53 years of work and man, it pays off. The monthly net deposits from in the bank accounts is $10,560 and that’s money that will not stop anytime. That’s way more than I made while working. And yes, a fellow once asked me, “how much would you have to have invested, to get that amount every month?” That’s a LARGE amount of paper wealth. I’ll take it!

Delayed gratification does work. Someone who wants to do it all NOW, as the insert says, will have a big chance of not doing it at all.

Paper wealth, huh? It’s amazing, the things people come up with to justify either not saving in the first place, or depleting whatever retirement funds they have managed to save so far.

Nice article, Bogdan.

I saw a virtually identical piece on “The Crunch” blog. Same points in same order, etc.

Is that you?, … or did he/she/they/it just copy your article ?

In any case it’s really good. I was tradIRA & SEPP_IRAs throughout my earning years after a military career. Now I’m well in RMD-land and trying to do ROTH conversions asap. Got nicked on my state income tax this year (1st time- $750). NY St doesn’t tax social security or military pensions! On further review it seems I was too light on QCDs and too heavy on the ROTH conversions. I’ve shifted 95% of our charitable giving to QCDs and will scale back the ROTH conversion a bit this year. The generous deductions under the current regime encouraged me to more ROTH than previously. Even so the tax bill isn’t onerous and I see that as a small price to pay to shelter more capital away from taxes. Keep up the good work.

Thank your your in-depth and insightful articles. They’re a big help with my planning!

Bogdan makes a strong case, and the “paper wealth” dismissal really is silly — the tax-advantaged compounding, the rebalancing flexibility, the Roth conversion ladders, the 72(t) and Rule of 55 escape hatches are all real and meaningful. Anyone in their 30s ignoring this is making an expensive mistake.

I’d offer one perspective from the other side of the milestone, though. Now that I’m retired and actually living off the portfolio, I’ve come to appreciate that the type of return inside these accounts matters as much as the tax wrapper around them. A balance that’s grown to seven figures on paper is wonderful, but it doesn’t pay the grocery bill until you sell something — and selling in the wrong tape is exactly what bear markets punish.

That’s why I’ve built my IRAs and taxable accounts to throw off durable, diversified income — managed credit, dividend-focused equities, and the like — sized to actually cover the lifestyle. The accounts are still compounding (through reinvestment), but the cash flow is real and arrives whether the market cooperates or not. Paper wealth becomes spendable wealth.

“That’s why I’ve built my IRAs and taxable accounts to throw off durable, diversified income — managed credit, dividend-focused equities, and the like — sized to actually cover the lifestyle. The accounts are still compounding (through reinvestment), but the cash flow is real and arrives whether the market cooperates or not.”

Milange, can you elaborate on how you’re taking the income your investment accounts are producing while also using reinvested distributions to compound the value of those accounts over time?

That sounds a bit like “having your cake and eating it, too” as the old saying goes. I’m interested in learning how you are managing to do both of those things at the same time.

Have you structured some of your accounts to produce income by throwing off dividends and interest while allowing other accounts to grow over time by reinvesting dividends and any capital gains distributions?

I agree with the benefits of creating income producing portfolios to provide spendable income in retirement. In some cases I think that’s a viable investment strategy that can be helpful to retirees, although many Financial Advisors tend to favor using “Total Return” portfolios to provide retirement income by selling investments to create “dividends” to live on.

Do you have a “secret sauce” that lets you “kill two birds with one stone” to get current income AND long-term growth at the same time?

Excellent article Bogdan. I am trying to teach all my Grand Children about the IRA’s and Roth’s, and the mighty power of compounding and the enemy of inflation. Take any % of Free Money. OK live now, fine, but what happens to those people when they reach my age of 80! Keep teaching our youth the real lessons of Finance. Thanks.

Regarding Rule 72(t), I’ve also read that you can break up a large Traditional IRA so that you have more control over the Traditional balance you choose to utilize for the Rule 72(t). For example, if you have a Traditional IRA balance of $500K but only want to Rule 72(t) half of it, you could split the account into two separate $250K IRA’s, leaving one alone and setting up the Rule 72(t) on the other.

I have a tentative plan to retire at some point in my 50’s, with the exact age very much determined by how the market cooperates between now and then. I’ll use Roth contributions (regular ones I’ve made and Traditional to Roth conversions I plan to make in the few years leading up to retirement), as well as taxable investments. If there’s a shortfall to cover my expenses, I’ll partition some of my Traditional IRA funds and set up a Rule 72(t) to generate enough income to cover the shortfall.

In terms of access or liquidity, you could also have mentioned plan loans, how a 401k plan with loan features, “done right”, can serve as the “Bank of Bogdan”:

Contribute pre-tax,

Defer federal/state income taxes,

Get employer match (on deferred taxes too),

Invest,

Accumulate,

Borrow to meet immediate need,

Rebalance investments to treat the plan loan principal as the fixed income investment it is, earning the plan loan interest rate,

Continue contributing while repaying the loan,

Rebuild the account for a future, greater need.

Repeat as often as necessary up to and throughout retirement.

Of course, individuals wouldn’t borrow from the plan where there was a better source of the needed funds.

To minimize distributions from loan defaults at/after separation, some plans allow for electronic banking, so that not only can payments continue after separation, but the term vested and retired participants can initiate loans.

For the past 18 years, plan loans that have been repaid (and ~90% of plan loans ARE repaid) have improved BOTH retirement preparation and household wealth.

Here’s how:

First, almost all plan loans were deemed by the borrower to be superior to other financing alternatives, such as where the plan loan interest rate is less than the interest rate that would have applied to a loan from a commercial source, and

Second, since 2008, almost all plan loan interest rates have been 5% – 7%, which far exceeds the return on all fixed income investments in the plan.

So, again, if you remember to treat the plan loan principal as the fixed income investment it is, by rebalancing your account to your target allocation after taking the loan, the plan loan will generally improve BOTH your retirement preparation and your household wealth.

Certainly worked for me.

See this nearly 20 year old study from the New York Fed:

https://www.federalreserve.gov/econres/feds/new-evidence-on-401k-borrowing-and-household-balance-sheets.htm

Do mortgage brokers consider retirement accounts assets for the purpose of loan eligibility or interest rates?

If it’s not useful for this, it’s a strong argument that it’s not even paper wealth; it’s deferred wealth.

Reading social media can be very depressing, but I’m addicted. The number of people who present themselves as clueless is incredible.

Just today I read a 40 year old woman who could not figure out where to invest in her 401k and asked if she should just put her money under a mattress. Part of her excuse for getting to this point was that she hated billionaires🤷🏻♂️

Investing can be complicated, but there is no need to not invest at a basic level and there is always information available and easy to find, if a person is interested, especially when dealing with an employer plan.

King Richard! Yes, if people don’t get any knowledge from home, they have to learn from …out there and who knows what kind of wacky ideas they latch on to.

It seems the most ill financial savvy folks are the most boisterous.

Incredible. Yet we see people make comments (worse yet, decisions!) based on their own personal biases or feelings all the time on social media.

I agree with the points about the tax advantages of IRAs and other tax-deferred accounts. One “tax” disadvantage that I do not see mentioned very often is that RMDs may trigger Medicare IRMAAs.

They may. The price of success. If there were no IRA investment and gains were being taxed through a lifetime instead of deferred potentially as late as age 75, I’ll bet the total hit would be far bigger than that from IRMAA.

Excellent article

AliceMia’s social media post is another reason why I have no social

media accounts. Her position also reminds me of comments that I have heard over the years by people, even very successful professionals and entrepreneurs, that the stock market is just a “casino.”

Bogdan explains the value of retirement plans very clearly, as usual.

AliceMia misses the larger point: The money that she will use to “make moves” and have “freedom” when she’s older had better remain untouched until that time. If she spends it now, she won’t have it to spend later. The retirement accounts she disparages are great vehicles to keep that money safe until that later time, as you point out. Nice article.

I agree that thinking of retirement accounts as wealth only on paper is missing the big picture. However, I also remember early in my career, when we had childcare bills for 2, a mortgage and a car payment…gosh it was hard to lock that money away!

16 years later: our house is paid off, we still have that Subaru but my daughter drives it now, college expenses have replaced childcare. Our Roth IRA’s earnings now outweigh the contributions!