FREE NEWSLETTER

I TURNED AGE 64 over the Labor Day weekend. One of my goals for my 65th orbit of the sun is to really dig into Medicare.

Luckily, I have a few friends and relatives who have blazed the trail before me. I’ve also studied Medicare as part of some financial planning courses I took a few years ago. Still, one topic I’ve never researched in detail is Medicare’s income-related monthly adjustment amount, otherwise known as IRMAA.

Traditional Medicare is made up of Part A (hospitalization), Part B (doctor’s services, outpatient costs and medical equipment) and Part D (prescription drugs). Parts B and D have monthly premiums. For 2021, the Part B standard monthly premium is $148.50. Part B also has a $203 deductible. After you meet your deductible, Medicare typically covers 80% of your Part B costs. Meanwhile, the Part D standard monthly premium varies based on the plan you choose.

IRMAA is an amount you may pay in addition to your standard Part B and Part D premiums—if your income is above a certain level. The Social Security Administration has a series of income brackets that determine what that amount is. Most people will pay just the standard premium amount. But if your modified adjusted gross income is above the specified threshold, you may owe IRMAA.

You can review 2021’s Part B monthly premiums by heading here. The IRMAA increase for Part B starts at incomes above $88,000 for single filers and $176,000 for joint filers. The surcharge for Part B can take your 2021 premium from $148.50 to $207.90—and perhaps as high as $504.90. The increase is per person, so married couples are looking at double these amounts. Meanwhile, the IRMAA surcharge for Part D starts at $12.30 a month and increases to $77.10 at the top income bracket. The Part D surcharge uses the same income brackets as those used for Part B. You can review the Part D amounts here.

When you sign up for Medicare, you’re provided with an initial determination of your costs, including whether you’ll have to pay IRMAA. The premium surcharge is usually based on your income from two years earlier, so 2021’s surcharges are based on your 2019 modified adjusted gross income. If it’s determined your income is above the threshold, you’ll be sent a notice explaining IRMAA in detail.

A friend of mine enrolled in Medicare this summer. Although he retired from fulltime work four years ago, he still does some part-time consulting. His consulting income for 2019 was high, so his modified adjusted gross income for that year was also high, especially for a single filer. His initial determination showed that his monthly Part B premium for 2021 would be $475.20, an increase of $326.70 a month—equal to $3,920.40 a year—over the standard premium.

He was concerned because 2019 was an outlier, unlikely ever to be matched again. Due to COVID-19, he had very little consulting income in 2020, and 2021 looks to be a slow year also. He doesn’t intend to ever work as many hours as he did in 2019. Basing his IRMAA on 2019’s income struck him as unfair.

His initial determination notice explained Medicare’s process to appeal if he thought his IRMAA surcharge was unfair. My friend claimed a life-changing event. In his case, the event was a work reduction. Other acceptable life-changing events include marriage, divorce, death of a spouse and loss of a job. He filled out Form SSA-44, and requested a letter from his employer describing the reduction in work and providing an estimate of his 2021 income. He then submitted these documents to the Social Security Administration. Within a few weeks, Social Security responded, reducing his IRMAA surcharge. IRMAA is recalculated each year. For my friend, Social Security will use his 2021 estimated income to calculate 2022’s IRMAA surcharge and then, for 2023, use his actual 2021 tax return.

As my friend’s situation makes clear, avoiding large IRMAA surcharges is another of the tax topics that retirees need to consider. Your modified adjusted gross income is determined by taking your adjusted gross income from your tax return, and adding back any tax-exempt foreign income and any tax-exempt interest. In my friend’s case, he now knows how much he can work to stay in a lower IRMAA bracket. Doing things to reduce your modified adjusted gross income, such as qualified charitable distributions in your 70s or later and Roth conversions in your 50s, can help reduce your taxable income during retirement, possibly allowing you to avoid IRMAA.

Be careful with those Roth conversions. Many folks use their early retirement years to covert part of their traditional IRA to a Roth. But if you’re in the tax year that includes your 63rd birthday and hence you’re two years from starting Medicare, a Roth conversion could lead to steep IRMAA surcharges. Also keep in mind that IRMAA is a so-called cliff penalty—meaning that, if you move up to a higher bracket by just $1, you’ll be hit with the full amount of the higher surcharge.

Richard Connor is a semi-retired aerospace engineer with a keen interest in finance. He enjoys a wide variety of other interests, including chasing grandkids, space, sports, travel, winemaking and reading. Follow Rick on Twitter @RConnor609 and check out his earlier articles.

Richard Connor is a semi-retired aerospace engineer with a keen interest in finance. He enjoys a wide variety of other interests, including chasing grandkids, space, sports, travel, winemaking and reading. Follow Rick on Twitter @RConnor609 and check out his earlier articles.

Want to receive our weekly newsletter? Sign up now. How about our daily alert about the site's latest posts? Join the list.

One of the shocks I experienced from IRMAA was not my fault. The SSA calculated my IRMAA back in the middle of the COVID lockdowns, and then a year later came back and said that it had not had current information at the time and had updated the IRMAA calculation. They informed me that I was being dinged for a large deficiency. But the real shock was that the SSA letter said that my Social Security payment would be docked 100% effective immediately, and I would continue to receive $0 – nada – until the entire deficiency was made up. That took a few months. I could muddle through, but it seems to me that the process is punitive. The SSA should allow Social Security recipients to continue to still have some portion of their monthly payment sent to them while an IRMAA deficiency (remember, not caused by them) is eliminated. (It certainly does not seem controversial, and would rank at about a 2 on the 10-point college student loan forgiveness meter.)

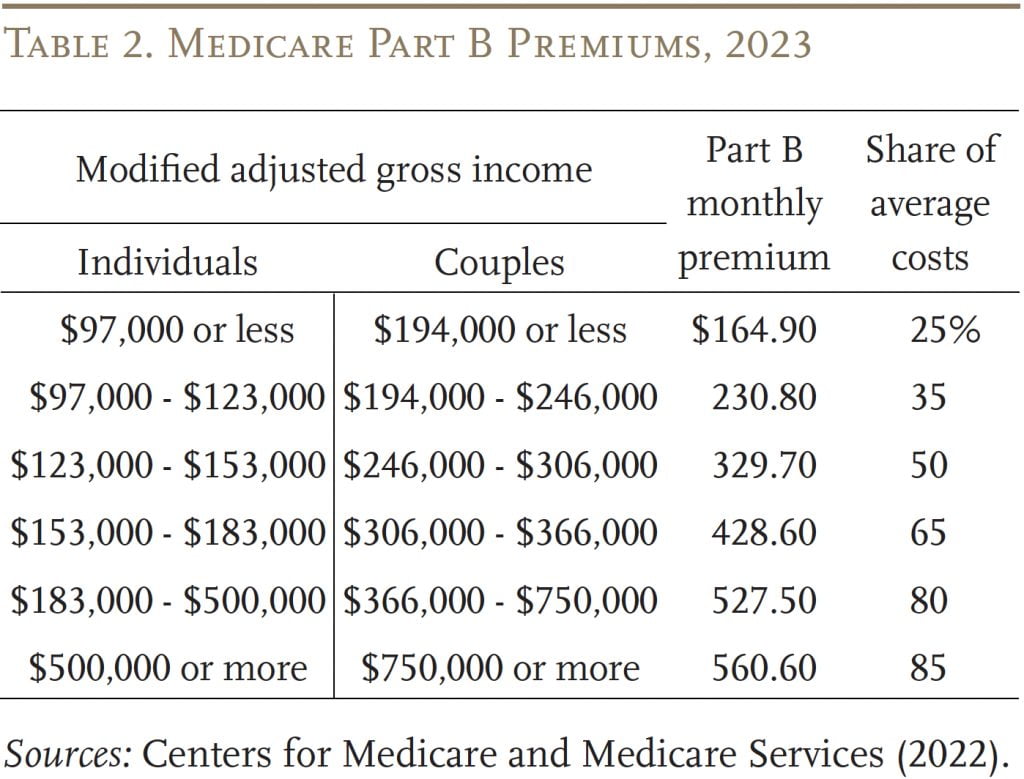

This is a helpful chart to explain how Part B is paid for:

.webp

.webp

Part B is financed by a combination of participant premiums and general revenues. Most beneficiaries pay the standard premium amount, which is set by law to equal 25 percent of the estimated average per-person cost; the remaining 75 percent is covered by general revenues. Beneficiaries with annual incomes over $97,000 ($194,000 per couple) pay a higher, income-related premium, reflecting a larger share of Part B spending, ranging from 35 percent to 85 percent of the average per-person cost (see Table 2).

The SSA 44 link in Rick’s article has changed. This is the new URL:

https://www.ssa.gov/forms/ssa-44.pdf

Thanks, David. I made that fix.

Thank you to Richard for this article and thank you to Jonathan for HD! My father passed away in 2021 and my mother sold property (not her primary home) that same year. She received a letter from Social Security near the end of 2022 showing that her 2023 Social Security payments would be reduced because of IRMAA due to the higher income reported on the 2021 tax return resulting from the capital gains. After I helped my mother file her 2022 taxes, we submitted form SSA-44 using the tax information from 2022 instead of 2021. She received backpay for the IRMAA amount withheld since January 2023 and her new monthly payment increased by nearly $200. Not a bad rate of return for a few minutes filling out the form! I’m pleased to report that the local Social Security office was very efficient and helpful in processing the claim.

That’s fascinating that your mother was able to escape IRMAA surcharges that resulted from the sale of a non-primary residence. An HD writer wasn’t so lucky:

https://humbledollar.com/2021/01/price-of-success/

The difference is that my mother met one of the qualifying life-changing events: she became a widow the same year of the sale. The property was sold after my father passed away.

Would the sale of a home be an approved life changing event?

That’s not listed among the life-changing events on this form:

https://www.ssa.gov/forms/ssa-44-ext.pdf

I will have to begin taking RMDs in 2025 and that will push my income into the first IRMAA tier, but I won’t have to pay because they will be basing it on my 2023 income. When 2027 rolls around will they bill me retroactively for the two years they missed?

IRMAA is recalculated every year based on your income two years previously. Thus, your 2025 income will only affect 2027.

There is something uniquely frustrating about

the IRMAA surcharges. 75 Pct of Medicare

Part B is paid for through the income tax

So if someone is in a higher bracket they

are already contributing in a progressive

manner to fund the benefit. Is it really

necessary to pay twice ?

Some retirees are now also paying the

Obamacare investment tax. A retiree might

feel it is expensive enough to pay for your

own health care and they should not have to

pay for other people’s health care.

All of this is taking place in a period of

ultra low interest rates where safe returns

to cover core expenses are non existent.

Actually 75% of Medicare Part B is paid for through PAYROLL tax, not INCOME tax. IRMAA is just a means test on recent income to reduce the subsidy received by higher income individuals.

Do not believe this accurate

payroll taxes are dedicated to

Part A – Hospitalization

Part B is the 25/75 mix of

premiums and General revenue

Great article. One minor clarification: where you state “married couples are looking at double these amounts” only applies if they’re filing jointly. Married couples who file separate taxes not only use the single amounts, but they jump immediately from the lowest to the highest bracket if they exceed the income of the lowest bracket. A real penalty if a married couple is filing separately.

Great point. thanks

I will add that when people request the information from there employer that they also ask for the disclosure about Medicare part D creditable coverage. While many employers put that in the open enrollment materials, get the most recent for the medical plan where you are enrolled.

Great article, Rick. This is a complicated subject and yours is one of the best explanations I’ve seen.

I did an SSA-44 appeal after I retired based on the life-changing event of an end to employment income and had success. It was a bit of work but not too bad and well worth the effort.

Great discussion Richard! I have one (minor) quibble; it’s my understanding that computing MAGI for IRMAA purposes, the non-taxable portion of Social Security benefits is not added back to AGI.

Now, if you were talking about MAGI for the purposes of computing the ACA premium subsidies, then yes, it would be added back in. This MAGI is different than that MAGI, which is also different than the MAGI for determining the destructibility of IRA contributions 🙂

Yikes, what a nightmare of convoluted math and acronym alphabet soup, thanks for helping us sort through it.

Thanks to you and Jonathan for clarifying this. I remember it was challenging to find the definition of MAGI for IRMAA. It’s good to know the various definitions.

Seems like another piece of faulty government logic. Income is income in determining affordability of spending money, but not in this case. I can understand the 15% not taxable because in theory that’s the overall percentage that workers contribute to Social Security benefits and is a return of taxes paid, but excluding the 50% is not, that’s true income. No use trying to figure tax law logic.

Thanks for pointing out the issue with MAGI. I corrected the story. On page 2 (after the cover page and table of contents) of the document below, there’s a chart with the gory details:

https://sgp.fas.org/crs/misc/R43861.pdf

I’m paying more to Medicare for Part D than I pay the company from which I buy the policy. Since I skipped my RMD last year I expect the cost to be lower in 2022 but it won’t last. All those people thinking they will get free medical care when they finally get to 65 have no idea…. Between premiums and an expensive medication my costs are higher than when I was working.

My wife and I are very fortunate to have most of our health care covered through her retirement benefits. The NYC Health Benefits program covers our Medicare B for $20/month and also fully reimburses IRMAA premiums, regardless of the bracket (the 20/month was just added beginning in 2022). The union that represented her as a City University of NY professor covers our Part D costs with a 20% co-pay for non-generics. We no longer complain about the high dues she paid for many years.

My employer dropped our retiree coverage for 2021 and we had to buy new coverage with HRA money. Part D was the biggest shock for so many retirees. Some went from paying a few dollars a month to hundreds for the same medication. Selecting a Part D plan is the worst part of Medicare because it is so variable based on the medication taken or that may pop up in the year after making a selection. Without a comparison tool that uses ones actual medication being taken, the comparison is impossible.

You can make the comparison on medicare.gov, using your actual medications (I also make it on my ex-employer’s site). The real problem is that you cannot change during the year even though your medications may well change. This is particularly unfair as the insurer may change the formulary during the year. The medication I take is Tier 5, prior approval required, so I stay with the same company and worry that they will drop the drug entirely. I am certainly a dead loss to them.

I just checked medicare.gov. Switching to different plan from the same company (Wellcare) will save me $2,000 a year, provided the approval carries over.

A good article on a complicated and misunderstood topic. I too have been paying high IRMAA premiums for years and hopefully always will – I’ll explain.

I frequently read the gyrations people plan to go through to avoid such additional premiums, including keeping their income below certain levels, Roth conversions before retirement, etc. SOME OF these people I read on Facebook are the same ones who rant about others not paying their fair share and using questionable, but legal tactics to avoid paying higher taxes. Makes you wonder since means tested premiums seem like one of the few things the government has gotten right – sort of.

Don’t get me wrong, I’d rather not pay IRMAA premiums, but I’m not going to lower my income to avoid them. Hence my first comment. As an aside I also think it outrageous that some of the FIRE folks keep their incomes low after amassing millions in retirement funds and they get virtually free health insurance for their families as a result of generous – income only – based ACA subsidies. All legal, of course.

Each year my RMD jumps us into the next higher IRMAA bracket. Because I skipped the 2020 RMD in 2022 my wife and I will save a couple of hundred dollars a month and then back up again.

I’d like to be paying $158.50 for Medicare in 2022, but I will pay much more for the same benefits as everyone else has. I also paid $196,124 in Medicare taxes over my working life, much higher than the average person. I’m not sure that is unfair.

But what I do feel is unfair is that in the IRMAA calculation earnings from a ROTH are excluded but municipal bond interest is included. Both were started with after tax earnings, why should both not be excluded and why include the interest when in tax theory at least, the interest rates are low to benefit the municipalities?

Richard – Were you able to lower your 2021 premiums because of the “missed” 2020 RMD? I didn’t think that was one of the exceptions. I’m sure your 2022 premiums will be lower because of your 2020 tax return.

I doubt Congress realized how much IRMAA premiums would be reduced when it suspended RMDs in 2020.

Thanks for the thoughtful response. Using a MAGI from 2 years previous seems almost to guarantee you will pay high IRMAAs early, and then possibly go down. If you work full time until you retire and take Medicare at 65, and they base IRMAA on your MAGI at 63, then your salary will likely push you into a big IRMAA. But your income at 65 and beyond could be significantly lower. I assume that is why they have an appeals process that my friend was able to use. He is still going to pay some IRMAA, but his 2019 income was an aberration based on a unique production schedule for the company we consult with.

Thanks for the article. I foresee SSA-44 in my future.

I’ve been paying IRMAA for years. If you are retired, and have a decent income, you may have to pay it. I do keep my eye on the brackets, and try to keep my MAGI under $138K.

IRMAA is now adjusted for inflation, so the brackets will be going up. They will be approximately $94K/118K/$146K/$174K,$500K for 2022, double that for married filing jointly.

About 15% of retirees have incomes over $100K, and 5% have incomes over $200K.

Those numbers are for 2023 thresholds according to a site I look at that has a pretty good record of accuracy.

https://thefinancebuff.com/medicare-irmaa-income-brackets.html

That site predicts $91k/114k/142k/170k/500k for 2022. Will will know officially from Medicare in a few days.

What is the source of retiree income data?

Thanks Richard! Another excellent reason to also hold off on collecting Social Security to age 70!

Not sure I understand- at age 70 many people with pensions and social security can be hit with IRMAA. Then at 72 , add in RMD’s…

I’m not sure I understand that strategy.

He’s probably referring to the strategy of doing Roth conversions, and that adding SS benefits on top of that not only makes the benefits fully taxable (and probably in a higher bracket to boot) but taking those benefits then could also subject one to those nasty IRMAA charges.

Or, in the absence of conversions, just the fact that it’s usually sound planning to use money from qualified plans during your ’60’s to fund living expenses, in order to “buy” a larger SS payment at 70. This strategy has the additional potential benefit of lowering future RMD’s, which also helps avoid IRMAA.