FREE NEWSLETTER

IF YOU HAVE a Money Market Fund (e.g. VUSXX, VMFXX), Treasury fund (e.g. SGOV), or any other Treasury ETF (e.g. VBIL), you need to know how to report it on your taxes correctly. If you don’t, you are overpaying on your state taxes unknowingly.

How and why?

These funds hold U.S. Treasury Bills. Treasuries are exempt from state and local taxes. Of course, this only matters if you hold these funds in a taxable brokerage account, which most people do.

The broker sends you a 1099-DIV form, but it’s your responsibility to figure out how to report it on your taxes correctly. By the way, bad tax preparers can miss this sometimes, or if you self-prepare, this may be something you aren’t aware of (I hope most of you reading HumbleDollar are familiar with this!)

This is one of those areas where the reporting rules are technically simple, but the execution is where people mess up. The IRS gets their share regardless (since interest is fully taxable at the federal level), but if you don’t adjust properly, your state will too, even when it shouldn’t.

The 1099-DIV doesn’t break out how much of the dividend was allocated to Treasuries. The software also wouldn’t know how much based on the 1099-DIV. This means that you generally have to figure out how to report it (or ensure your CPA does it correctly).

Now, the 1099-DIV will have a breakdown of every single stock/ETF you have, but you have to find out the percentage of a fund that holds Treasuries.

This percentage is not on your brokerage statement. It comes directly from the fund provider (Vanguard, iShares, Schwab, etc), usually buried in their “tax center” or “year-end tax supplement” pages.

Let me give you an actual example.

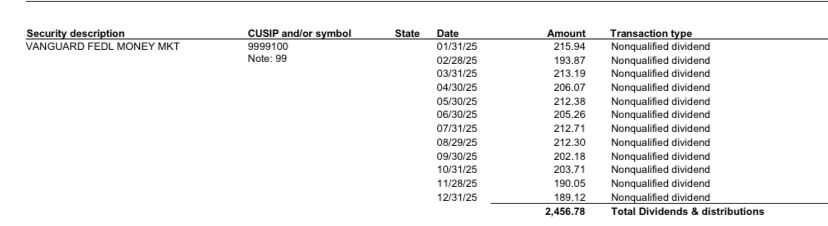

Say, in 2025, you received $5,000 of dividends from two funds.

Then, if you scroll down, you will see a “Detail Information” of your dividends:

We can see that $2,456.78 came from Vanguard Federal Money Market fund.

The entire $2,456.78 will be taxed at the federal level, but how do we figure out what’s taxed at the state level?

This is where the extra step comes is.

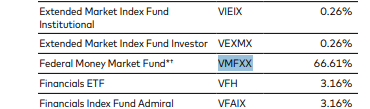

During the end of the year, the fund manager (e.g Vanguard for VMFXX) will post a “US government source income information” on their Tax page.

This report tells you what portion of the fund’s income is derived from U.S. government obligations (Treasuries), which is the key to the state tax exemption.

We can see that 66.61% of VMFXX holdings for the 2025 tax year were income derived from the U.S. government and, therefore, are not taxable at the state level.

So, we would take $2,456.78 * 0.6661 = $1,636. Of the total, $1,636 is derived from U.S. obligations, and you would only pay state taxes on the remaining ~$819.

That $2,456.78 is still fully taxable federally. This is strictly a state adjustment.

It’s also important to note that some states say “if less than 50% of the fund is from the U.S. government (like Treasury Bills), you can treat it as 0%.”

For example, California, Connecticut, and New York are some of these states. So, if the fund has only 35% coming from the Treasury, you shouldn’t even calculate the exempt amount for these states.

Now, if you buy Treasuries directly from TreasuryDirect, they will send you a 1099-INT, and you can just enter that information directly into the tax software. No extra calculations are needed. That’s because the income is already clearly identified as U.S. government interest, no allocation required.

So, how do you report that dividend interest calculation?

In most tax softwares, after entering the 1099-DIV, it will ask: “Did a portion of dividends came from a U.S. Government interest?’

So, you would just check it off/select and enter the amount from Treasuries ($1,636 in our example).

Behind the scenes, this flows into your state return as a subtraction or adjustment, depending on the state.

Some software might ask for the percentage of dividends that are state tax exempt. However, this is a bit tricky because you might receive other dividends in your brokerage account.

In that case, calculate the amount from the Treasury, say $1,636, and divide it by your total dividend amount (e.g. $5,000)

If you have someone do your taxes and you have some of these Money Market Funds or other Treasury ETFs, double-check your state tax return and see the amounts reported. This will save you some money. It’s also not too late to amend your tax return if this was missed.

Specifically, look for a “U.S. government interest subtraction” or similarly labeled line item on your state return. If it’s zero and you held these funds, that’s a red flag.

If you live in a no tax state, this would not apply to you, but still good to know in case you move!

I hope you found this one valuable.

![]() Bogdan Sheremeta is a licensed CPA based in Illinois with experience at Deloitte and a Fortune 200 multinational.

Bogdan Sheremeta is a licensed CPA based in Illinois with experience at Deloitte and a Fortune 200 multinational.

It seems that interest earned on direct obligations of the U.S. government (such as U.S. Treasury bills, notes and bonds) is generally exempt from state and local income tax. However, GNMA, FNMA and FHLMC securities are not included as U.S. government obligations.

Can someone please confirm the above information? What about interest income from Fed Farm Credit, Student Loan, TN Valley Auth, and other entities listed in the “Mutual Fund and UIT Supplemental Information” towards the end of a 1099-DIV from Vanguard? Can someone please clarify this important issue? Thanks.

Following is an excerpt from the State of California FTB Publication 1001, 2017, page 5:

“Federal law requires the interest earned on federal bonds (U.S.obligations) to be included in gross income. California does not tax this interest income. The following are not considered U.S. obligations for California purposes: Federal National Mortgage

Association (Fannie Mae); Government National Mortgage Association (Ginnie Mae); or Federal Home Loan Mortgage Corporation (Freddie Mac).”

Thanks for the tip. I live in New Jersey which does not recognize my use of a QCD. Therefore, I declare my RMD in NJ income that is not on the Federal return. The information provided in this article allowed me to receive $418 additional return from two (2) filed NJ tax returns using NJ-1040X. Both the NJ instructions nor TurboTax pointed out this tax reducing technique. I will use this in future returns. You just made living in retirement in New Jersey a little bit easier.

Thanks for the information. My screwup cost me a about $12.00 in state taxes but it won’t next year.

Thanks for the excellent column! I noticed last year (TY 2024) that our CPA had not subtracted U.S. treasury interest on our state return. We were able to fix this before submitting the 2024 tax return. But we were likely overtaxed by our state in earlier years. I’m surprised the very long “Tax Organizer” we receive in January from the CPA doesn’t catch this issue.

Thanks for this – I pointed out this issue to my accountant (didn’t review the draft return, just pointed out the potential issue), and got the following message back:

I have reviewed all of your 1099 dividend holdings and compared that to what we deducted on the Schedule S of the NC return. While some of the US Treasury interest was deducted on Schedule S, it appears as though we missed some mainly from the Fidelity account. The difference is about $18k more US Treasury interest that can be deducted on the NC return and about $700 of NC tax savings.

I’ll take $700 anytime. Thanks again!

I save the annual income source report to my tax folder, just in case of an audit and the report disappears online. Virtually all the cash in my taxable Fidelity account is in FDLXX. In 2025, ninety-seven percent of its income came from Treasurys, and the fund yielded only 0.05% less than their default money market (SPAXX).

Excellent piece, thanks.

Another technical detail – at least for California (and I believe NY) – is that the fund’s holdings from Treasuries must be greater than 50% at the end of each quarter. So please be careful to check that your fund satisfies this slightly stricter requirement.

Thanks Bogdan for this meaningful article, of something I never noticed before. Vanguard has a footnote #99 indicating: For the Vanguard settlement fund (9999100), the U.S government obligation percentage is 66.61%. For further information, please search “Tax information for Vanguard funds” on Vanguard.com. I must admit Humble Dollar continues to be a learning experience, and a very good one too.

Another potential tax-related pitfall involves reporting income from national muni bond funds on your state return. This is required in Colorado and probably other states as well You must add back the muni income from other states to your current state return. The percent of your in-state muni income (which is not taxable state or federal) should be listed on the back pages of your annual tax statement behind the 1099’s.

Thanks for the explanation. A technical clarification would be that Treasury Direct won’t send out a 1099-INT, but rather you would log into your account and pull the tax form. The menu flow is “Manage Direct”, “Manage My Taxes” and look for the correct year. There will be a form link if there were any taxable transactions for the year.

I especially found this extra bit of information useful as I live in an impacted state:

“…you can treat…”

Wonder why they don’t use the word “must”, instead? To me, “can” = “may”, making it a choice.

Very good advice! I wasn’t aware of this until my Fidelity rep mentioned it. As retired I have significant money in these types of MM. I filed an amended state return for ’25 and saved >$2,000 in state tax. I now know where to look and provide the % of federal holdings not subject to MN tax to my accountant.

Good info. Thanks.

Very useful, thanks! I’ll have to make sure I check this when filing 2026 taxes.

For 2025 Vanguard provided the US government source interest for each of my holdings as a footnote in my 1099 DIV. Made it a little easier this year.

This is true. But the H&R Block software that I use required that the dividend amounts on the 1099-DIV be reported as if they were reported on separate 1099s, and then entering the percentage from Treasuries on a following page in the questionnaire. So still a bit complicated, but as this excellent article points out, worth making sure it’s done correctly.

Fortunately, that’s all done behind the scenes in TurboTax. I download the 1099’s from Vanguard and TurboTax walks me through some questions where at some point I input the $ amount of US sourced income for each investment based on the percentages reported by Vanguard in the 1099.