FREE NEWSLETTER

MY COWORKER RECENTLY retired. He is 50 years old and has been with the company for over 25 years.

The company offers a decent 401(k) match (100% match on 6% of your salary) along with other great benefits.

In his case, how can he generate income? How can you retire early if most of your assets are in retirement plans?

Most tax-advantaged accounts have restrictions on withdrawals, but there are a few strategies that many people don’t know of:

Running the numbers

There are a lot of estimations on the safe withdrawal rate.

According to FireCalc, a 3.5% withdrawal rate (plus inflation adjustment) has a success rate of 100% for 30 years. While it’s not a perfect measure, it’s something that we can use as a baseline calculation.

So, for a $1.5M portfolio, you can withdraw ~$52,500/yr.

Say my coworker was able to get a $1.5M portfolio with the following split: $1M in a traditional 401(k), $300,000 in a taxable brokerage, and $200,000 in a Roth IRA.

What’s the withdrawal strategy?

First, I would probably roll over the 401(k) balance into 2 separate rollover IRAs (split 60%-40%).

This move would allow you to set up the “Substantially Equal Periodic Payments” (also called the 72(t) strategy) and avoid the 10% penalty on withdrawals. This plan would be established only on the 60% IRA.

There are three different methods (RMD method, fixed amortization, or annuitization) for calculating the amounts you can withdraw.

Using a 72(t) calculator, we can see that a $600,000 72(t) setup can result in a ~$36,969/year distribution, avoiding the 10% early withdrawal penalty.

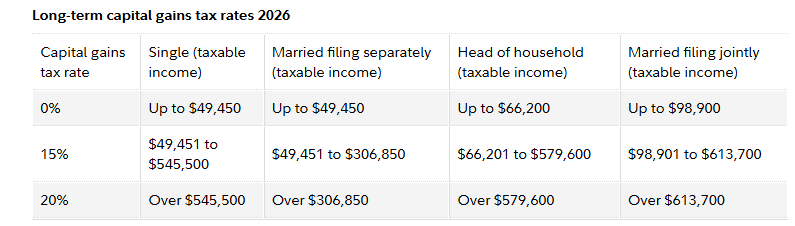

With $300,000 in a brokerage account (say invested in $VTI), we are looking at ~$3,720 in dividends (~95% of them will be qualified). Since our taxable income will be below $49,450, most will be taxed at a 0% rate.

In addition, say that the $300,000 portfolio had 75% of it in capital gains and 25% in basis.

We can sell an additional $10,500 of VTI per year and will have $7,875 of long-term capital gains, taxed again at a 0% rate.

So far, we’ve pulled $36,969 + $10,500 + $3,720 = $54,189 of cash. This would put us right at around a 3.5% safe withdrawal rate.

In addition, while not needed in this case, you can also minimize your 72(t) withdrawal amount (by rolling over less into the account to be subject to the rules) by withdrawing your contributions from the Roth IRA.

Contributions can always be withdrawn penalty-free at any time (different rules apply to earnings/conversions, though).

Taxes

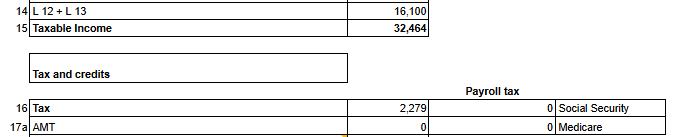

From the tax standpoint, he’ll pay ~$2,279 of federal tax in 2026:

(Assuming single, no kids)

This is ~7% effective tax rate.

Because the tax rate is very low, it may make sense to withdraw less from the brokerage account, and increase the 72(t) withdrawal. This can help prevent future RMDs, and can help with step-up in basis for his heirs.

Depending on the state, you might also pay no state taxes, either on full income, or partially on capital gains and/or retirement income.

What about health insurance?

One of the benefits of controlling your portfolio withdrawals is that you can predictably estimate your income. While the enhanced premium tax credit expired as of 2025, because of the lower income you may be able to qualify for subsidies on the state level.

Social Security Benefits

Before Social Security benefits (SSB) kick in, you can also do Roth conversions to further reduce the size of the 401(k) (and lower your future RMDs) and move more money into a Roth IRA.

Withdrawals from a Roth IRA don’t count toward provisional income for the SSB tax calculation, allowing you to minimize your tax liability.

In addition, controlling your income will allow you to be below the IRMAA (Income-Related Monthly Adjustment Amount) threshold. This surcharge increases Medicare Part B and Part D premiums for higher incomes but doesn’t apply to income below ~$100,000.

![]() Bogdan Sheremeta is a licensed CPA based in Illinois with experience at Deloitte and a Fortune 200 multinational.

Bogdan Sheremeta is a licensed CPA based in Illinois with experience at Deloitte and a Fortune 200 multinational.

Thank You!! More articles like this please! I have/had 4 sets of patents. Based on where all 4 couples have ended up, well into their 80s they could have retired sooner or could have/could spend more. I know this is because of the fantastic economy we have lived in over the last 40ish years of their lives. That may be vastly different the next 40. But if it is bad we will all be financially hurt in ways we can’t predict today. What is the value of living an independent life as soon as you can? Or giving when alive instead of living in fear of running out of money? I don’t know the answer but I’m very interested in more stories on early retirement or giving!

Have a partner who works. A simple solution.

My dad hated his job when he was 55. My mom was a med school professor and just got a grant for a few years. I was successfully launched into my career so I was off their books.

She told him to quit.

How does the Standard Federal income tax deduction, $16,100 plus a bonus amount of $8050 for people over 65 totaling $24,150, affect this scenario? If one earned $49,450 + $24,150 in capital gains and qualified dividends, would the Federal tax bracket still be zero?

Perhaps I’m missing something. If the individual retires at 50 and plans for 30 years of spending, then the plan ends at age 80.

I’d like to note that “FIRECalc will assume you want to keep your annual spending about the same for as many years as you specify, you aren’t planning on receiving any Social Security or pension, and your retirement portfolio is invested in a “couch potato” portfolio of 75% stock index and 25% bond funds, with a 0.18% fee to the fund. ” (Spending is inflation adjusted). How the portfolio is invested is adjustable and other income sources can be included (social security and pensions).

If they retire at 50 and a 3.5% withdrawal rate is enough to afford a comfortable lifestyle for them, this person is in extremely good shape. As Bogdan points out, they are looking at 100% success rate based on all historical 30-year periods. If you bump this up to a 50-year retirement, they still maintain a 94.3% success rate based on all historical 50-year periods.

This is before inputting social security benefits into their future income sources. To me, this is not leaving too much to chance as others suggest. This is simply the case of someone having enough to retire far earlier than the norm and people being spooked by it.

I appreciate the mention of FIRECalc. It’s by far my favorite basic retirement calculator.

Great summary, but I think this fellow needs a part time job. If the Stocks Gods are good, no problem. Insurance can be a killer, I pay about $20,000 per year at 80 years old. Inflation is a bigger killer. Personally I would not retire on this scenario without some additional income.

This analysis would lead me to work longer! I see no reason why this person’s health insurance should be subsidized for a lifestyle choice. And what happens at age 80? My husband and I are both 83 and still need money.

I think the post is very interesting— and agree with the comments about needing a professional to run the numbers.

Thanks for the rundown, Bogdan. I share Dick’s concerns about the uncertainties the future brings. The person in your example might be cutting it close. Hopefully, your 50-year-old colleague has a more robust portfolio that allows a lower withdrawal rate to meet expenses.

Also, it could be wise to keep a toe in the game by keeping professional licenses current, maybe do a little free-lance work? When my wife left full- and then part-time work after our daughter was born, she kept a PRN gig for a few hours per month just in case she needed to quickly jump back as a primary earner. After nearly two decades, she’s close to hanging it up at age 60.

But these are the thoughts of a cautious man. Perhaps your friend couldn’t face another tax season? I understand. Most jobs tend to cycle through periods of happiness and horror. Sill, gaining perspective from a long look into the future bolstered my strength to face many Monday mornings.

With that being said, I appreciate your analysis of a good way to generate income while avoiding problems.

This is a good example of the value to be had by hiring a qualified professional to provide unemotional retirement planning. Thanks for detailing your process, great analysis, Bogdan.

Of course, if I were the client in this exact scenario, I probably would have been disappointed with the amount of income I could safely generate, so probably would have decided to delay my retirement. Your advice would have been worth much more than your fee.

“…hiring a qualified professional to provide unemotional retirement planning.”

There is a financial planning firm I know of that requires all of its employees in the firm to have their own planner, including the owner.

I thought this article by NAPA (National Association of Plan Advisors) provides interesting reasons why some use, or don’t use, a planner.

https://www.napa-net.org/news/2021/3/why-consumers-useand-dont-usefinancial-advisors/

I’ve never used a planner, but in the area I live now, people tell me they have a financial planner.

I think that, for all the talk here about ‘doing it ourselves’, most of the population needs a pro. The scary part is, how does that person assess “qualified”.

So helpful to see that hypothetical carried out. Thank you!

Don’t think we will know that for 25 more years.

This is a worry free, reasonably secure retirement?

I think the impact of health insurance is oversimplified and understated.

30 plus years at the mercy of the stock market, tax laws and assumptions for success and needing to keep income below certain levels.

No thanks.

Not quite retired, but close. I’m going with this approach as many do: saved all my life, have a sizable nest egg invested in a diversified portfolio (equity/fixed income) + a solid SSB, will implement a comfortable SWR and rebalance. No guarantee, none of us have that.

Perhaps it is a “Lean FI” situation.