FREE NEWSLETTER

SEQUENCE-OF-RETURN risk has long been a major concern among retirees—and it’s a real danger right now for those who just quit the workforce or soon will. Also known simply as sequence risk, it refers to the chance that the market declines sharply, forcing retirees to sell investments at depressed prices to generate income.

Wade Pfau, a leading retirement researcher, published a paper highlighting the danger involved. As he makes clear, a few years of market losses coupled with portfolio withdrawals can decimate savings, increasing the risk that a retiree will run out of money.

You might view sequence-of-return risk as the opposite of dollar-cost averaging. Instead of buying more shares when stock prices are down, you’re selling additional shares at lower prices to generate the same amount of income.

This year, unfortunately, provides a good example of how market forces can affect retirees’ savings—and their plans. Consider a retired couple with a $1 million portfolio who need $50,000 a year from savings to cover their expenses.

If they withdraw $50,000 at the beginning of the year, their balance is reduced to $950,000. If the stock market returned 10% that year, their balance at the end of the year would be $1,045,000. If this continued year after year, the retired couple would be in great shape. By the end of the fifth year, their balance would be $1,274,370.

But what if the market declined 10% in the year when they made their initial withdrawal? At the end of that first year, just as the couple was about to withdraw another $50,000, their balance would be $855,000. What if this continued? At the end of five years, their balance would be slashed by nearly 60%, to $406,211.

Folks who retired during the 2008-09 Great Recession encountered this risk head-on. I had a colleague who reached retirement age in 2007. He had changed employers several times in his career, so—unlike many of his coworkers—he didn’t have a significant pension. He also had major education expenses, including putting a daughter through medical school.

His plan was to work for as long as possible, continuing to save and invest. He also planned to postpone claiming Social Security so his benefit would grow in value. Unfortunately, the NASA program he was working on was canceled in 2008, eliminating his job. It was a stressful time for my colleague. Fortunately, after a few months, he was able to find a new job and continued working into his 70s.

Today, my wife and I are also confronting sequence-of-return risk. My wife retired last year, so 2022 is our first year with limited earned income. I have a pension that covers a good portion of our annual expenses, but we expected to dip into our retirement savings for the discretionary extras. Over the past two years, we’ve also undertaken several major home renovations.

We’d planned for these expenses by holding a large amount of cash, equal to about three years of discretionary expenses. The renovations ate up about two years of this money. This worries me some, but I remind myself that this is why we worked hard and saved all those years.

When we both claim Social Security in about five years, the combination of my pension plus our Social Security benefits should easily cover our expenses, as well as the extras—travel, gifts, entertainment—that make for a pleasant retirement.

How can we counteract sequence-of-return risk? The hope, of course, is that the market turns around and starts on its next bull run. But if luck isn’t with us, here are five ways to structure retirement income to lessen sequence risk’s corrosive effect:

1. Annuitize. If you’re lucky enough to have a defined benefit pension, you have a guaranteed stream of income. You get paid no matter what the market does. If you don’t have a pension, you can create an equivalent version by purchasing income annuities. This transfers investment risk from you to the insurance company.

2. Cash bucket. This is a popular strategy, one that my wife and I are using. It hinges on the notion that the stock market rebounds within a reasonable period of time. If you have enough cash to cover, say, three or five years of expenses, you can weather the market’s down years—usually.

3. Reduce spending. You might trim or delay large purchases. For many, tightening their belt comes naturally during a market downturn. But during the current market swoon, it’s been made more difficult by today’s high inflation. Recall the example above, where our hypothetical couple withdrew $50,000 a year. For next year, they might need more like $55,000 just to keep up with rising costs.

4. Work. For many retirees, a second career or part-time work can fill idle hours and provide welcome income. This can reduce or—if you’re industrious enough—even eliminate the need to sell investments in a down market. Indeed, it’s a strategy I’m considering. I’m currently looking at a few consulting opportunities.

5. Social Security. Some retirees plan to delay claiming Social Security until age 70 to maximize their benefit. If your retirement nest egg is getting scrambled by a prolonged market slump, you might opt to claim Social Security earlier and thereby reduce portfolio withdrawals.

Part of my angst about retiring into a down market is that I simply hate tapping our hard-earned retirement savings, especially at reduced valuations. But as I keep telling myself, why did we save all this money if not to fund our retirement? I doubt I’ll ever stop worrying completely, but I’m getting more comfortable with this “decumulation” phase.

Richard Connor is a semi-retired aerospace engineer with a keen interest in finance. He enjoys a wide variety of other interests, including chasing grandkids, space, sports, travel, winemaking and reading. Follow Rick on Twitter @RConnor609 and check out his earlier articles.

Richard Connor is a semi-retired aerospace engineer with a keen interest in finance. He enjoys a wide variety of other interests, including chasing grandkids, space, sports, travel, winemaking and reading. Follow Rick on Twitter @RConnor609 and check out his earlier articles.

Want to receive our weekly newsletter? Sign up now. How about our daily alert about the site's latest posts? Join the list.

Decided to go back to work after being fired due to my on the job accident. Long story. After two years of being home, wife suggested I find something part time. By the next day, got a part time gig in the rental car business and now, over ten years later, am still in that industry. Went from an independent contractor to an employee at two of the largest rental companies out there. As an independent contractor, my schedule was erratic & never knew when I was going to work until the night before. I longed for a set schedule and after a year, found such a position.

We live off my pension for the big things with the wife throwing in some as she’s a professional working full time. Took s s at 64 as being a retired federal worker, I only get a small fraction of it due to that ridiculous Windfall Provision Act of 1984, which is totally unfair & needs to be reversed honestly! She’ll take s s at age 70 in a couple of years which will hopefully go into the joint account with my pension. We’ve always lived under our means and taught the kids the same, which I am happy to say they all do. Paying off the mortgage by working as much overtime as I could helped us retire it almost 28 years ago, made a huge difference. Am able to bank my part time salary and have been doing some dollar cost averaging these past few years. Have a handful of dividend paying stocks which keep on paying me monthly.

Once we retire, think we’ll be just fine. Depending on my health, we’ll do as much as I am able. Looking forward for a long & happy retirement in a few years!

I also waited until I could claim the maximum Social Security benefit, and it has made a big difference. But that strategy might not be for everyone – one example might be if health is a concern or if there is a family history of early mortality, or one doesn’t have enough financial resources or income to bridge the waiting period to FRA or beyond.

Another thing that sometimes is ignored is the time it takes to manage a portfolio, do tax planning and RMD withdrawal strategies, especially as one ages, or if another person has to take over management of the individual’s or family’s financial affairs, or the level of interest and expertise one has in managing these aspects, vs. devoting time to other interests and activities in retirement.

Also, to echo some of the other comments, there does seem to be a lot of software focused on the pre-retirement accumulation phase, which isn’t all that helpful when you’re more or less past that period. I was already using a spreadsheet to track income and expenses, but kept looking for software that would allow the user to make projections using future assumptions about income, expenses, rates of growth/return, Roth conversions, RMDs etc. The one that came closest to what I wanted was spreadsheet based and looks a bit “old-school” but has been very helpful once all the data is gathered and entered. One thing I like about it is that I can create pro formas with different financial assumptions. (Note that I have no connection to this company or to any of the people involved with it; am just mentioning it in case it helps someone else 🙂 https://www.completeretirementplanner.com/ )

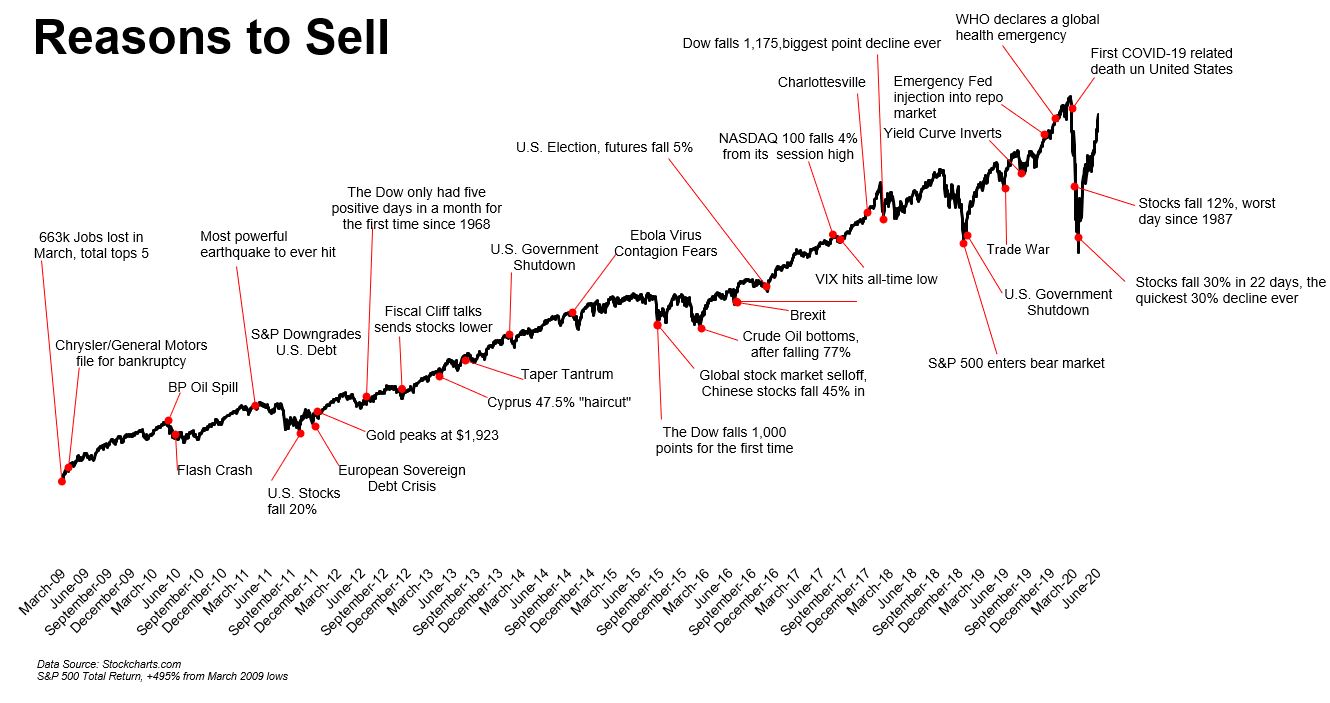

During accumulation I kept this chart close to remind me that more people lost money avoiding risk than embracing it.

[URL=”https://theirrelevantinvestor.com/wp-content/uploads/2020/06/reasons-to-sell-6.10.2020.jpg” [/URL]

[/URL]

During decumulation I think cash-flowing assets are going to be increasing vital to mitigate SORR. Pension, SS, SPIA,MYGA, depreciation protected rents, qualified dividends, futures options.

>> “more people lost money avoiding risk than embracing it”

Yep, that is the central fact I keep in mind too. It’s amazing how few seem to acknowledge this.

Yeah, SORR is a giant PITA. Especially lately where we get high market volatility coupled with high inflation – so that cash stash you’re sitting on declines in real value by the day. Add to that the spectre of a recession, further tanking the market, and you have a perfect storm for decumulation retirees. Like me.

Check out Michael McClung’s book, Living Off Your Money. In it, he explores this topic exhaustively, looking at various approaches and how they would’ve fared over all the 30 year retirements since the 1920s.

Ultimately he ends up recommending an approach called Prime Harvesting, which uses a straightforward algorithm to determine what side of your portfolio to withdraw from (stocks or bonds), and when to replenish the bonds.

Three months from retirement, and two more years before claiming SS. I’ll be living off a bridge-fund (cash) and my first IRA distributions until then.

(And also making big Roth conversions in those two years of lower taxable income – one benefit of a big stock decline on the eve of retirement.)

I did not expect the party to go on in 2021, because every time the market rose several percent I took profits/shifted asset allocation to bonds.

Bonds? Two-year treasuries – like the host of this site I’ve been uncomfortable with anything longer for a while.

I did not forget the retirees of Y2K, socked by a crash and years of miserable returns, followed by another crash in 2008-09.

If need be I can spend-down that bond pile for 15 years without selling stocks. Even if stocks are still 50% underwater then, the sad remainder will carry me to the end, with a little left over for the heirs.

Social Security will cover all my expenses, so I don’t have to worry excessively about inflation. (I’ll worry about Social Security instead.) The portfolio is for the nice-to-haves, SS for the need-to-haves.

People with annuities are getting crushed by inflation, as usual, and it’s happening even faster these days. A fixed amount of money is meaningless because inflation makes any set amount worthless over time, so I don’t see annuities as a good solution.

A cash bucket is one solution, but it’s also needless mental accounting, and duplicative for anyone with a balanced portfolio. One can simply not rebalance into stocks in retirement, and accomplish the same thing without needing extra spending rules to manage a bucket. For example, a $100 60/40 portfolio after a 50% market drop has $30 in stocks and $40 in bonds (a 43/57 portfolio). Spending $4/yr (4% of the original portfolio) already means you’ll only spend from bonds until you’re back to 60/40. Even if markets stay flat after the drop, that would mean 5 years of spending only from bonds before getting back to 60/40 ($30 in stocks and $20 in bonds) and needing to then sell stocks. This works without needing a set of arbitrary decision rules for when to spend from, and how to ever replenish, a cash bucket.

When it comes to social security, I would suggest spending down bonds and cash first, to delay claiming it for as long as possible. The reason to hold any bonds and cash it to have something else to spend when stocks are down. Fully utilize that source of income before permanently cutting down what for most people is their only source of guaranteed inflation adjusted income.

I don’t understand how this math works in the current scenario. Many folks doing 60/40 own all or some nominal bond funds as their 40% – and they’re also down by double digits. So pulling from bonds is equally troublesome.

Unfortunately people (even professional financial advisors) often go way too far with duration risk, and experience what you describe. Total Bond Market funds have a duration of about 6.7 years, which is simply too long if it’s the only bond holding in the portfolio. However, you can mix in short term bonds, or even just a good money market fund; to get to a more stable overall duration. Since Money Market has a duration of zero years, if you want an overall 4 year duration, you could split your bonds 60% Total Bond Market fund, 40% Money Market (6.7×60% + 0x40% = 4.02 years). Substitute what you can from Money Market with I-Bonds each year, and you should be in good shape.

Without using a TIPS fund, 3-5 years is a reasonable range for duration. To find out your preferred duration, assume the fund price will swing by up to 3x the duration. So if your duration is overall 4 years, expect up to 12% in price swings. Vanguards VBTLX has a 52 week high/low of 11.41/9.58 (19.1%) and a duration of 6.7 years (6.7×3 =20.1%) so this 3x rule of thumb seems to be accurate.

Just also keep in mind, most of the time duration risk won’t cause price swings this severe, and returns will be reduced as duration risk is reduced, so don’t get overly conservative with duration.

Regarding TIPS, an overall 5-7 year duration could work if half of bonds are TIPS, but this is more of a personal choice. Intermediate TIPS will lose 10% for no immediately apparent reason (just because inflation expectations change) so they aren’t without their own problems. I prefer my bonds to be boring, so I don’t use TIPS, and offset lower expected bond returns with a slightly higher allocation to stocks. But for someone with less than 60% in stocks, holding some amount of bonds in TIPS would be a good idea.

My wife and I are actually doing most (I am one who is consulting) of these plus a couple more: We have a TIPs bond ladder matched against expenses, we have a HELOC and I worked “one more year” in my W2 job before retiring in 2018. We have not reduced expenses but we have delayed buying a car. I say we are doing most because we are still delaying SS and planning to do Roth conversions when I stop working before 72. Our retirement plan specifically addresses SORR, longevity, market and inflation risks.

What are you worried about, Richard, unless your portfolio won’t support another 5 years of withdrawals?

I’m aware that most people on this site are in or approaching retirement and as I approach retirement in the next 3-4 years, this topic is of concern to me as well. I read an article in Morningstar recently that I found very interesting. It may be of interest to your kids (or grandkids) as it discusses the SORR for those in the accumulation stage. I don’t know if it is accessible without a subscription, but the link is below.

https://www.morningstar.com/articles/1111697/retirees-arent-the-only-ones-who-face-sequence-risk

I saw the Morningstar piece when it came out. I loved it. Great context and perspective.

I was able to see the morningstar article you provided. It was interesting to see the inverse effort on a young saver versus an older retiree. It’s an interesting perspective and one worth sharing with younger folks. Thanks!

A portion of my portfolio has always been in dividend stocks. It’s an income that allows me to sleep well. Fortunately, selling stocks to generate income isn’t in the foreseeable future for me.

Very important topic which I’m always thinking about. Might consider early retirement in a couple of years, but the thought of running out of money due to bad timing/markets is quite scary.

For those of you who have played with calculators/programs that incorporate Monte Carlo simulation, would you share your suggestions on which ones to use in order to get a reasonable confirmation on whether or not one can ‘safely’ call it quits? Have tried the free ones from Fidelity/Schwab/Vanguard, but not comfortable w/ their different assessments. Thx.

I would suggest abandoning the safe withdrawal rate concept and use percentage of portfolio instead, and just plan around variability in withdrawal income. Withdrawing a reasonable percentage (3-4%) of the then-current balance each year is the only way to be 100% certain you won’t run out of money. You lose spending consistency, but gain spending efficiency. It does require tracking required expenses separately from discretionary expenses, so you know how much income variability to plan around, but that’s where I landed after thousands of hours of research.

Good article! This gets discussed often but it is important for people close to retirement to be informed about this topic. SORR can torpedo retirement plans and people need to know how to guard against that.

I planned to retire at age 64 in 2008. My timing was typical of my investment decisions. Ha! It was customary for department heads like me to announce their retirement well in advance. Fortunately, I did not do that. I got a major haircut from Mr. Market, so I decided to work a couple more years. That increased my pension, and I was able to add more to my savings.

I could have still retired and been fine but the extra two years provided a nice buffer, plus I enjoyed my job so there was no compelling reason to retire. I am very thankful I was able to delay my retirement.

When I retired five years ago, sequence of returns risk (SORR) was probably our family’s top financial concern. We put off retirement a few extra years until we were highly confident that our retirement financial plan could withstand a 50% market pullback in the first five years of retirement.

With today’s high inflation, SORR is definitely a concern for recent retirees. Here are a couple solid additional articles on SORR:

https://www.businessinsider.com/why-your-retirement-projection-is-flawed-2015-9

https://eversightwealth.com/one-portfolio-risk-to-rule-them-all/

This has been written about several times on HD, but as you mentioned Wade Pfau I would also point out he is an advocate of using Reverse Mortgages in one’s retirement plan, specifically the HECM to establish a large line of credit. He actually wrote a book about it called, “Reverse Mortgages: How to use Reverse Mortgages to Secure Your Retirement.” When used strategically and responsibly, this line of credit can help mitigate sequence of returns risk.

From FI Physician who reviewed Wade’s strategy (HECM line of credit) and found it to be effective. “In order to combat a negative sequence, draw on your line of credit in years when equities are down to avoid reverse dollar-cost averaging. Money from the line of credit is tax-free, which may be especially important if you are getting income from your fully taxable IRA or if additional ordinary income would increase taxation of social security or cause increased Medicare surcharges.”

From Wade’s book on using Reverse Mortgages in retirement: “Opening a reverse mortgage earlier in retirement and using it in a strategic manner is generally more effective than treating a reverse mortgage as a last resort option only to be considered when all else has failed.”

I have no experience using an HECM, but I do think it is something I will strongly consider in the future. I understand there are going to be higher origination fees and higher interest expenses added to the loan balance if I draw on this line of credit, but I also assume that paying off the line of credit after stocks recover will mitigate the higher interest expenses, and that the higher origination expenses would be worth it to combat sequence of return risks throughout my retirement.

I was going to get a home equity line of credit while still working, with any eye toward a future opportunity to expand my homestead post-retirement, but was turned away by the seemingly high cost of establishing it at the local bank.

I’m far more likely to open/maintain a traditional HELOC before retirement than a reverse mortgage/HECM.

You could do that, but then you’d have to start making immediate monthly payments on your HELOC loan balance. A HELOC is still a valuable tool to have in retirement, but as it relates to sequence of returns risk mitigation, the HECM is more useful.

I’m one who retired during the Great Recession and waited to claim Social Security. Money was tight for a while, but with my income relatively low, I was able to convert my traditional IRA to a Roth, decreasing the amount of taxable RMD’s I’d have to take in the future.

Sadly, I believe too many folks are unable to find a way to reduce their spending in down market years and consider making up for it in the up market years. It’s funny how some discretionary expenses all of a sudden become fixed. Of course many don’t even budget in the first place.

If I was in this situation I know I wouldn’t handle it well. Heck, I worry each day I look at my accounts and see a decline and I’m not touching the investments except for RMDs.

I often wondered if withdrawing not annually, but monthly or even bi-monthly would help mitigate the problem, kind of the reverse of regular investing. My Fidelity account has the ability to do that and transfer money to my bank account.

The other possibility I think about is having a portfolio with sufficient dividend paying stocks and bond interest. Count on that income instead of selling from the account. Again, Fidelity allows me to select by investment which are reinvested or not and I can switch at any time.

I’m beginning to wonder if retiring before ones SS FRA is ever a good idea. I bet there are more than a few retirees thinking about that now.

I would love to find a calculator that does what you suggest–one that models what portfolio balances look like over time when taken as a proportion of the account’s current asset allocation percentages, either monthly, quarterly, or annually. I’ve been considering such a strategy, starting by using a Single Life Expectancy Table, and maybe switching to the Uniform Life Table once RMD’s kick in. I have yet to find such a calculator; while annuity calculators abound, specific ones that address these kinds of scenarios seem few and far between. The Federal TSP website used to have one that used an inputted rate of return, combined with the two tables mentioned above. But when they switched to the “improved” system earlier this year it’s disappeared, unfortunately.

It seems that nearly all info related retirement calculators that I can find is for accumulation. For the decumulation phase, you’re kinda on your own.

Many of my friends claimed Social Security as soon as they could. I thought it was a bad idea and I’m glad I waited.

That’s not always the best idea though.

Unless you can afford to do it with no meaningful hit to your lifestyle/spending as you wait.

(I know – you’re referring to those who can’t afford to do that.)

I have turned off dividend reinvestment on my taxable accounts. Between dividends and interest my cash needs are met. If I have extra cash, I can use the funds to rebalance my investment mix.

I am beginning to suspect that the middle-class retirees, who have to make withdrawals from their retirement accounts, will be in a lot of trouble in ten or fifteen years. They just don’t have the skills to manage a pool of capital assets well, and often they don’t have enough assets anyway.

I would not have retired at age 61 if I did not have enough money to live on my income, and not have to withdraw principal.

“I would not have retired at age 61 if I did not have enough money to live on my income, and not have to withdraw principal.”

That’s an enviable position to be in – but if the rest of us in America had to wait for that level of savings, 99 out of 100 of us would be forced to work until we died on the job. No thank you.

Not touching principal – aka the perpetual portfolio – is the extreme end of conservative. Your heirs will certainly thank you and enjoy spending all that moolah, but I sure hope others who cannot reach that level don’t hold themselves to this standard – how sad that would be.

If a potential retiree can get by on a 2.5-3% withdrawal rate for a generous life expectancy timeframe, they can almost assuredly weather the worst economic storms, short of a catastrophic black swan like US govt meltdown.

At some point, time is far more valuable than money.

What do you mean by “middle class”, and why are you sneering at them? I would say I am middle class (although that might be my English upbringing showing). I retired at 53, twenty-two years ago, and have yet to touch my portfolio for more than a few thousand, and not every year. I will finally start withdrawals when I move to a CCRC next year, but they should not even reach 4%.

“I am beginning to suspect that the middle-class retirees, who have to make withdrawals from their retirement accounts, will be in a lot of trouble in ten or fifteen years.”

Yeah, especially when you consider that there are some big-name self-appointed finance guru’s out there telling people that they can reasonably expect a 12%+ annual return on their assets, and that an 8% withdrawal rate is just fine. Wonder what that portfolio will look like in another 10-15 years?

That’s ridiculous – nobody with any financial savvy would believe that. You might as well buy the CEF or BDC that’s paying 10% – what could possibly go wrong?

Rick, you are just a few years ahead me, and write about topics that are on my mind. Thank you for this one.