FREE NEWSLETTER

WHERE YOU PUT your investments can make a huge difference for your after-tax wealth.

As you know, we have 3 main investment accounts:

Asset location

Say, as part of your investment strategy, you want to start putting money in bonds. You have a 401(k), Roth IRA, and a brokerage account. Where do we put them?

Brokerage account

When you hold bonds, like BND (Total Bond Fund ETF), you pay taxes on non-qualified dividends (e.g. interest from the bond) up to a max rate of 37%, plus net investment income tax, if applies. This means that if you receive $1,000 from the bond, you will pay approximately $370 in taxes if you are in the highest tax bracket.

Of course, not all of us are in such bracket, and perhaps a more reasonable number would be ~$220-240 for most people. But is taxable brokerage the right choice for you? Not really. You would be paying $200+ every year, plus state/local taxes.

Personally, I’m 100% invested in equities, because I want to be aggressive with my portfolio in my 20s, but if I did have bonds, I wouldn’t hold them in a brokerage account.

Roth IRA/Roth 401k

When you purchase bonds in a Roth IRA, you will not pay taxes on the interest since it’s a tax-free account!

That’s much better than the $200+ in taxes you would pay in a brokerage account.

But is it the best choice? Well, bonds are considered “fixed income” funds, and they don’t grow much. Since Roth IRA is a tax-free account (meaning we pay no taxes when we sell these investments), we want as much growth as possible in it. Bonds would hinder that performance.

So, holding bonds is better than brokerage, but likely not the most ideal place.

Traditional 401(k)/403(b)

By holding bonds in an account like a traditional 401(k)/403(b), the interest income avoids immediate taxation, compounding tax free until withdrawal.

So, we avoid the ~$200+ of taxes and aren’t sacrificing the tax-free compounding like we are with a Roth IRA. This makes the pre-tax 401(k) the perfect location for bonds.

Of course the 401(k)/403(b) choices are limited and are provided by your employer. So, if they don’t offer a bond fund, you might not have a choice.

Some other examples:

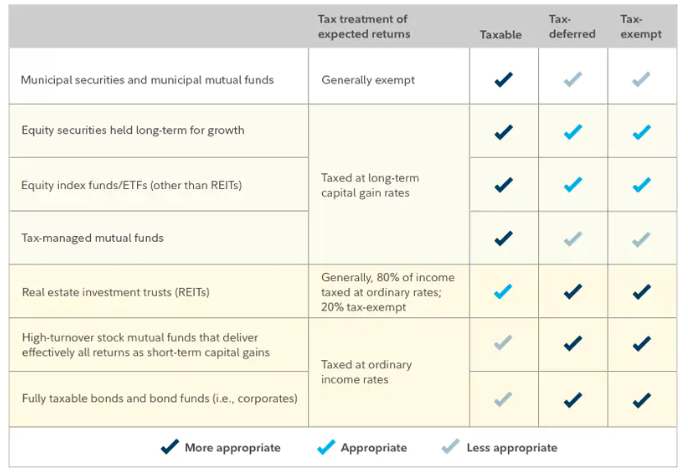

I really like this visual from Fidelity to reference:

But how much does this matter? Vanguard’s research finds that a thoughtful asset location strategy can add significantly more value than an equal location strategy. The value added typically ranges from 5 to 30 basis

points of after-tax return, depending on circumstances (e.g. income, portfolio size)

Overall, I hope you think about all of your investments & how they get taxed.

![]() Bogdan Sheremeta is a licensed CPA based in Illinois with experience at Deloitte and a Fortune 200 multinational.

Bogdan Sheremeta is a licensed CPA based in Illinois with experience at Deloitte and a Fortune 200 multinational.

Great analysis, Bogdan, thank you.

We are in the process of converting all of my wife’s traditional to a Roth before claiming Social Security. All of the Roth funds are in 100% in Vanguard Total International ETF. Our portfolio allocation is balanced in our traditional accounts. We are maxing out our income using conversions up to the top of the12% tax bracket. Our tax rate will be the same in the future, but the purpose is to obtain tax free growth with funds that may never be tapped, and thus will be inherited tax free. This will also decrease our RMDs, and allow us to better control our taxable income.

Hi David.

By putting Vanguard Total International ETF (VXUS) in a Roth you cannot claim the foreign tax credit (FTC) even though you are paying foreign taxes. I make a similar decision when I have my Vanguard Global Equity index fund (VTWAX) in my traditional IRA account as my thinking resulted from my decision that I currently prefer the re-balancing simplicity over the modest FTC I am giving up by doing so.

I have been thinking that about five years out from now that when my wife is done with her traditional to Roth IRA conversions that I will then use my unspent (hopefully) RMDs distributions to buy VXUS in a taxable account to be able to claim credit for those withheld foreign taxes and my heirs will eventually be likely to get a step up in basis of those equities in my taxable account.

I would be interested in your thinking and planning to have VXUS in a Roth.

David, you may want to diversify the Roth by adding US equity.

I follow what the author says. Where you put your investments is very important.

Our equities and ETFs are in brokerage accounts. The fixed income part of our asset allocation is all in my IRA.

When working I put my savings in tax deferred rather than Roth accounts (wasn’t available early on in lower earning days). I don’t think we qualified for Roths anyway because they had income limits.

The tax savings was great because of the higher tax bracket I was in. Now that I’m retired I’m in a much lower tax bracket so it turned out well.

Converting to Roth accounts now would create too much of a tax consequence. The time to do it would have been after I retired and put off SS,which I did not do. I took it at FRA at 66.

In hindsight, I probably should have waited until age 70 and converted some IRA to Roth accounts.

Our income is 2 SS checks and RMDs, along with capital gains (very moderate) generated from the taxable account, This is more than enough to pay our bills. We planned it so that we have no fixed bills other than our real estate tax. No mortgage, no auto loans, etc.

We are nowhere near the $212k IRMAA limit, which will be raised to $218k in 2026.

The taxable IRA is quite large, but we only take out the RMD requirement. When we pass, our kids will have to pay taxes on the inherited IRA, but our taxable trust accounts are much larger and all the gains will be tax free to them. In an ideal world they would be inheriting a Roth with no taxes.

There’s a problem with your choice between a Roth and a tax-deferred account.

Assume that you save $1000 at 5% for 20 years and your tax bracket is 20%. For the Roth, you would have $800 initially and after 20 years of compounding you would have about $2123 tax free. With the tax-deferred account, you would have $1000 initially and after 20 years you would have $2653 before taxes. If you are still in the 20% tax bracket, that would be $2123 after taxes, exactly the same as the Roth.

The Roth/tax-deferred comparison mostly depends on your tax bracket when you remove the money from the account. There are also some tax situations, like IRMAA when the tax-deferred withdrawal would increase your tax, while the Roth would not.

Good analysis Bogdan.

My IRA was my working 401k so I didn’t have much choice over the investments. It’s mostly index funds, but there is a bond fund as well.

Our brokerage account has two stocks, index funds and several municipal bond funds tax free state and federal.

Not sure I’m doing it most efficiently, but at this stage it doesn’t matter that much. I have no hope of escaping IRMAA no matter what I do.

Good topic Bogdan.

In a 11/20/2025 podcast of The Great Retirement Debate series, CPA’s Jeff Levine and Ed Slott discuss this similar topic. Their episode titled ‘Should you invest your IRA differently than your taxable account’ mirrors your points to a large extent.

My personal experience with asset location decisions has been I found it hard to decide to pay more tax currently by funding a Roth type retirement accounts and not using the available traditional tax deferred retirement accounts (IRA, 401(k), etc.) for a larger portion of my retirement savings. It is now harder to do a good job with asset location when I failed to save in the type of account (Roth) that allows future earnings to be earned tax free. I give myself a little grace in that Roth accounts did not exist until half way through my working career.

At age 75 I currently find myself in the tax situation where every additional dollar of ordinary income causes an additional $0.85 of our social security benefit income to be additional taxable income thus making Roth conversions currently more tax expensive than if I had made Roth contributions/conversions before my social security benefits began.

I additionally worry that if I do not currently convert some to a Roth that if I die before my four year younger spouse that she will be stuck with a much higher tax rate in the years after I am gone.

With the 7/4/25 OBBBA tax law changes now in place I am modeling and plan to take action for tax years 2025-2028 to make sure that I utilize the current tax laws to hit my taxable income target with my goal to minimize our expected tax obligations for the remainder of our life.

I have read that the best time to get shade by planting a tree is 20 years ago, the next best time is today. Trying to take my own advice.

Bill, my father used to tell a story about his grandmother from when she was in her early 90s. She wanted a peach tree planted in her yard. Her family advised against it, arguing that she wouldn’t live to pick fruit from it. But, she insisted, convinced that she would. She turned out to be right, and enjoyed those peaches before she died.

Ed, It’s wonderful that your great-grandmother was able to enjoy peaches from the tree that she planted, and I admire her determination! I just want to mention that the story is at least 2000 years old–it’s in the Talmud, where an old man is planting a carob tree, which requires 70 years to become fruit-bearing. Nevertheless, he eventually is able to enjoy the tree’s fruit, as can his children and grandchildren, etc. The real point of the story is that we do things for the people who come after us, just as those who came before did for us. The same applies to investing and accumulating wealth: it’s great to build for our own later years, but perhaps even more satisfying to know that we’re planting trees for our children.

Thanks for the reference, Tom. I’m pretty sure my great-grandmother didn’t get her inspiration from the Talmud, but the similarity illustrates how thoughtful, optimistic people separated by time and distance can arrive at the same good conclusions.