FREE NEWSLETTER

EVERY DAY, I READ about the Federal Reserve’s thinking on interest rates—increase, hold, decrease—and the possible impact on the economy. But what about the impact on savers?

As someone who has most of his non-stock monies invested in taxable certificates of deposit, high-yield savings accounts and money market funds, I have a different criterion for the right interest rate: It’s the rate that would give me and other risk-averse savers a modest real return of perhaps 1% a year, after adjusting for inflation and taxes.

Unfortunately, after doing a few simple calculations, I’ve realized that notching this seemingly modest real return requires a rare combination of interest rates, tax rates and inflation rates.

Suppose a couple has “moderate” income—meaning 2023 taxable federal income between $89,450 and $190,750—which puts them in a 22% marginal federal tax rate. If we add an assumed 3% marginal state tax rate, that gives them a 25% total marginal rate. As shown in the table below, our hypothetical couple would achieve a 1% real return if they earned 4% interest with 2% inflation. Think of that as the “Goldilocks” scenario.

By contrast, with a 1% interest rate and 2% inflation—which was fairly typical pre-pandemic—the real return was quite negative. Hoping higher interest rates will drive that 1% real return? They won’t help if they’re accompanied by correspondingly higher inflation rates, plus taxes are assessed on the nominal interest earned, not inflation-adjusted interest earnings.

Yes, it’s better to have more income than less. Still, with a lower income, your chances of making a 1% or better real return on savings are higher because your marginal tax rate might be just 15%. This 15% assumes a couple has 2023 taxable federal income between $22,000 and $89,450, which would then be assessed at a 12% marginal federal rate, with maybe a 3% state tax rate on top of that.

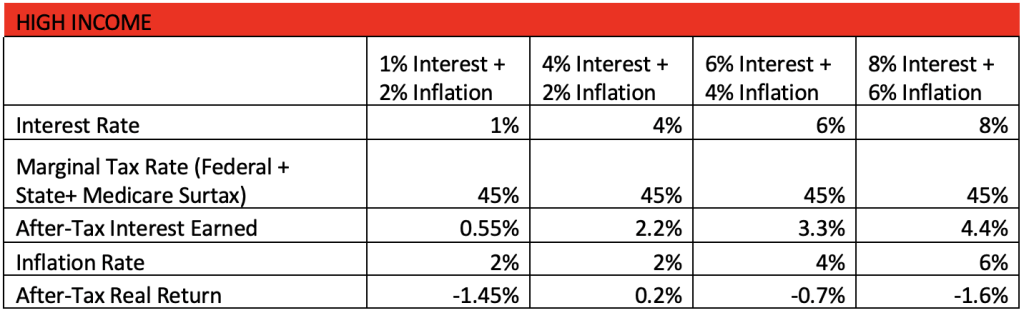

On the other hand, if you’re fortunate to earn enough to reach the highest marginal tax rates, your chances of earning a 1% real return on savings are pretty low. This is due to a marginal tax rate of 45%-plus. Where does that figure come from? A couple with 2023 taxable federal income of more than $693,750 would face a marginal federal rate of 37%, plus a Medicare investment income surtax of 3.8%, plus an assumed state tax rate of 4%-plus.

The lesson: While everyone’s circumstances differ, in general it takes a decent rate of interest, coupled with a low tax rate and a low inflation rate, to earn a real return on low-risk taxable savings. That doesn’t mean you shouldn’t hold cash investments for upcoming expenses and financial emergencies. But you won’t get rich holding your long-term investment money in cash.

After 40 years working for GSK Consumer Healthcare (now called Haleon), Paul Sklar took advantage of a severance opportunity and left the firm in 2022. He now does part-time consulting as Paul Sklar Consulting LLC. In his spare time, Paul likes to exercise, read and spend time with his adult children.

After 40 years working for GSK Consumer Healthcare (now called Haleon), Paul Sklar took advantage of a severance opportunity and left the firm in 2022. He now does part-time consulting as Paul Sklar Consulting LLC. In his spare time, Paul likes to exercise, read and spend time with his adult children.

Want to receive our weekly newsletter? Sign up now. How about our daily alert about the site's latest posts? Join the list.

Remember, when you pay down the mortgage by adding extra dollars, say monthly so you can pay it off early, you are in effect stuffing money in your walls. A house you live in is not an investment. It’s a place to raise the family and place of comfort and serenity.

Last time I looked I couldn’t sell the bathroom for a Viking River Cruise or sell the basement for the granddaughter’s education at SMU.

I love running a hypothetical using the S&P 500, or a a few funds we have had for decades, with the $400 a month extra going to the prepayment of the 30-year mortgage. Rolling 30-year periods starting in 1937 shows what $400 initial and the same monthly for 30-years yields in total return.

Investing in the greatest companies in the world has proven to be a fabulous place to create wealth. But, you time, patience, and discipline.

So true and so unfortunate!

After reading this article, I was wondering how/if you achieved a real return of 1% in the years before Covid when the Fed rates were zero?

I remember the days when the Prime rate was 21%, and MMFs were paying 15% and inflation was almost 15%. We weren’t making 1% on cash then either and tax rates were much higher than now. I am not sure that making net 1% on our cash consistently is possible or even necessary. Having some cash gives you freedom and security. It is a necessary thing, and as such, you just have to do the best you can at any point in the interest rate cycle to minimize what you will inevitably lose by having it.

Stelea99,

Thanks for your reasonable question/comment. For clarity, I wasn’t asserting I personally had always achieved a 1% real return on risk-free cash equivalents, only that I thought this was a reasonable aspiration I would be happy to achieve.

Your question inspired me to do a very crude analysis of historical annual real cash returns from 1947-2022. In this analysis, I loosely estimated the average prime rate in each year and included the average CPI inflation rate in each year. Then, I made the very challengeable assumptions that the best risk-free cash returns for the year might have been 70% of the average prime rate OR prime rate minus 2 points. I generally selected whichever of these yielded the lower cash return except when the cash return would have been zero or negative. I made another challengeable assumption of an average 25% marginal tax rate on the cash return to calculate the after tax return and then subtracted the inflation rate.

Across the 76 years analyzed, 38 (half) of the years generated negative real returns after taxes and inflation. The worst individual year was 1947 when inflation was quite high (14.4%, perhaps due to post World War II effects), but the prime rate was only 1.75% resulting in, according to my methodology, very negative cash returns after taxes and inflation. The worst decade was the 1970s when my calculated real returns after inflation were negative in every year. And 2021 and 2022 were pretty bad also.

I freely acknowledge my analysis is crude and contains readily challengeable assumptions and methodologies. Still, it does suggest to me that generating a real return on risk-free cash cannot be easily achieved consistently over time – although I wish this were possible.

I would be happy to share the spreadsheet I created with you or any other HumbleDollar reader, but I’m not sure how to do that. If you or other have any interest, perhaps Mr. Clements has a way to either post the spreadsheet or otherwise share.

Illustrative of how hard it is to stay ahead of inflation. That’s where the TINA (there is no alternative) to stocks idea comes from.

Thanks for the article.

Many of us in retirement and who have claimed a social security benefit find our self subject to the tax torpedo which results in each dollar our taxable social security benefit becoming taxable at a much higher marginal rate for each dollar of other taxable income.

The details are well described by Jonathan in the guide – https://humbledollar.com/money-guide/taxes-in-retirement/

I try to control the cash/bond interest type income I earn outside of tax deferred or Roth accounts by holding those taxable investments in I bonds where I can chose the year when I recognize that taxable income.

Thus my primary focus is controlling the income tax part of my bond / cash investing as it can take the biggest bite out of my nominal interest earnings.

This seems a smart strategy. I’ve not invested in I bonds, but the ability to choose when to recognize their taxable income seems an argument in their favor.

Seems like an argument for paying off ALL debt with extra money.. since there is no tax on that savings! (Except for a few people who can take the mortgage interest deduction).

Personally, I feel more comfortable with no/minimal debt, but “rationally” it depends on the rate of interest you’re paying on the debt and the after tax interest yield you would otherwise achieve on the money you could use to pay down the debt. For example, if you are lucky enough to have a 3% mortgage and are in a 25% marginal tax bracket, a 4% risk free (insured) CD would yield 3% after tax and you’d “break even” investing in the CD versus paying down the mortgage. In this example, if you could earn more than 4% risk free, investing in the CD would return more than paying down the mortgage. However, if you could earn less than 4% from the risk free CD or your mortgage rate were above 3% (new rates today are about 7%), paying down your mortgage would be a better “investment”.

Of course, there’s an alternative school of thought that you shouldn’t pay down your mortgage because you could earn more investing in the stock market, but since the stock market isn’t a risk free investment, that’s an apples versus oranges comparison and a separate asset allocation/risk tolerance discussion.

In your example, you’re assuming that mortgage interest isn’t tax-deductible — which is true for many folks today, because the standard deduction is now so much higher. But the numbers would be different if readers are able to itemize their deductions.

You are right. Based on Jaime’s comment, “Except for a few people who can take the mortgage interest deduction”, I did assume the mortgage interest would not yield a separate tax deduction. But certainly with a large enough mortgage and/or a high enough interest rate, large mortgage interest payments could cause a person/couple to itemize instead of using the standard deduction and deduct mortgage interest at the margin.

A good argument for definitely holding cash in tax-protected accounts, and selling more tax efficient stocks from taxable accounts when you need cash, offsetting by buying in the tax-protected account. Jonathan has more on this somewhere in the guide I believe, but I couldn’t find it to link to.

I believe this is the section of the money guide you’re thinking about:

https://humbledollar.com/money-guide/municipals-vs-taxable-bonds-in-a-retirement-account/

Yes that’s it, thanks Jonathan.