FREE NEWSLETTER

WE CAN’T CONTROL the financial markets. But we can pretty much guarantee we’ll pocket whatever the stock and bond markets deliver—by buying index funds. So why do I hear so much grousing from indexers?

At issue isn’t a failure of index funds, but rather a failure of investors’ expectations. Over the past few months, I’ve heard from countless hardcore indexers who have done the sensible thing and built globally diversified portfolios. Often, they own some variation of the classic three-fund portfolio: a total U.S. stock market index fund, a total international stock index fund and a broad U.S. bond market fund. Yet they have a gnawing sense of unease—because their portfolio hasn’t kept up with the U.S. stock market averages.

As stocks have soared while interest rates have bumped along at miserably low levels, many investors have written to me, questioning the need to own bonds. More recently—and, to me, more troubling—the disdain has extended to foreign stock markets.

As stocks have soared while interest rates have bumped along at miserably low levels, many investors have written to me, questioning the need to own bonds. More recently—and, to me, more troubling—the disdain has extended to foreign stock markets.

This, of course, smacks of performance chasing. Over the past five years, the S&P 500 has clocked 13.1% a year, while MSCI’s Europe, Australasia and Far East index has eked out a 5.9% annual gain and the Bloomberg Barclays Aggregate Bond index has managed just 2.3% a year. The past few weeks will, no doubt, further fuel investors’ discontent. Foreign stocks have taken it on the chin, their prices knocked down by turmoil in Turkey and a strengthening U.S. dollar. The latter cuts the value of foreign shares for U.S. holders.

What we’re seeing, however, is more than just performance chasing. From the comments I’ve received, there’s a pervasive belief that U.S. stocks are both safer and offer higher returns, and that foreign stocks are both riskier and destined to underperform. I’ve heard from folks who complain about sketchy accounting and weaker property rights abroad, which suggest foreign stocks are a dodgier proposition. In the next sentence, they’ll tell me that international markets have always underperformed and will always underperform. They then go on to say that they can get all the foreign exposure they need with U.S. multinationals, which they happily acknowledge perform just like U.S. stocks.

Got all that? Maybe it’s time to revisit first principles—and recall both the reasons we diversify and the unbreakable connection between risk and reward.

When we spread our investment bets widely, we’re looking for both short- and long-term portfolio protection. In the short-term, owning thousands of securities from different parts of the global market will give us a less volatile portfolio, as some securities zig when others zag. Meanwhile, over the long haul, global diversification increases the odds that we’ll meet our financial goals, because there’s less risk our portfolio’s performance will be badly derailed if one or two parts of the financial markets post truly wretched returns.

We won’t get this short- and long-term protection if our sole investment is U.S. stocks, including U.S. multinationals. Nothing is going to zig when our U.S. stocks zag, so we lose the short-term portfolio protection. What about the long haul? We’ll be sunk if the next decade sees U.S. stocks sink.

That brings me to the contention that U.S. stocks are both safer and sure to outperform over the long term. I find this bizarre. Remember, these comments are coming from folks who have drunk the Kool-Aid, accepted that markets are efficient and banked their life’s savings on index funds.

If we accept that markets are efficient, we’re buying into the notion that all parts of the financial markets have similar risk-adjusted expected returns. True, those expectations almost certainly won’t be met: Some market segments will do surprisingly well, while others will disappoint.

Nonetheless, our starting assumption should be that risk and expected return are joined at the hip. We shouldn’t start with the idea that one market—the U.S. stock market, in this case—is not only safer, but also pretty much guaranteed to deliver superior returns. If that were the case, rational investors everywhere would buy U.S. stocks, driving up their price and eliminating this free lunch.

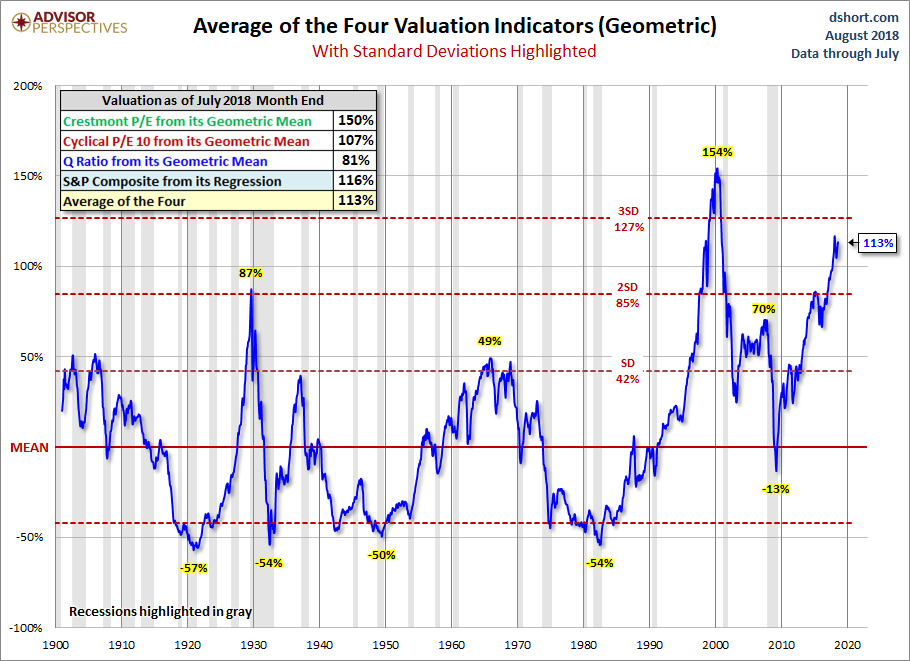

This raises an obvious question: Are U.S. stocks in a bubble? I am loath to even mention the word. I feel we’re too quick to slap the “bubble” label on any asset that’s recently performed well. Much of the time, bubbles are only apparent later, when we look back and marvel at the magnitude of the comeuppance and clearly see the folly that preceded it.

But bubble or not, many U.S. investors—including many indexers—are displaying an alarming degree of home bias. U.S. stocks may offer comforting familiarity. But they’re also more expensive than other major markets, and they alone don’t make a good portfolio.

I believe every investor should look at his or her investment mix and ask, “What if I’m wrong?” What if U.S. shares are priced so richly that a decade of terrible performance lies ahead? I’m not predicting it will happen, but I can’t be sure it won’t—and I don’t want the consequences of that potentially terrible performance to nix my retirement. That’s why I have roughly a third of my portfolio in U.S. stocks, a third in foreign stocks and a third in bonds. I won’t end up with the greatest returns. But I’m pretty confident I won’t end up broke.

Follow Jonathan on Twitter @ClementsMoney and on Facebook.

Want to receive our weekly newsletter? Sign up now. How about our daily alert about the site's latest posts? Join the list.

I agree with what you say about diversifying internationally; however what do you think of the argument that if the US market takes a dive, the rest of the world will divetoo? Also, what about Jack Bogle’s advice not to invest in Int’l?

Finally, would you agree that, from the perspective of a non US investor, having a market cap weighted World ETF is still a ‘bet in favour of the American market’ as this Economist article points out,

https://www.economist.com/finance-and-economics/2017/04/08/americas-disproportionate-weight-in-global-stockmarket-indices

so that it’s probably a good idea to havle less than 50% of one’s equities in the US stock market if you are lookig to retire in Europe?

In the short-term, if US stocks dive, foreign markets will follow suit. In that scenario, if you want to limit losses, you need to own bonds. I hate to disagree with Jack Bogle on anything, but I disagree with him on foreign investing — for all the reasons I express in the above article and more. My inclination is to mimic the global stock market in my own portfolio, which means having roughly half in US stocks and half abroad. My only concern, as someone approaching retirement, is the currency exposure. I will spend most of my savings on US goods and services, just as folks retiring in Europe might end up spending much of their savings on goods and services denominated in Euros. You can partly limit that currency exposure by owning bonds denominated in your local currency. But I think there’s a case for having part of your stock market money in a fund that hedges its currency exposure — especially if your domestic stock market makes up a relatively small part of the global stock market, which would be the case for everybody except those living in the US.

Thanks for getting back – I imagine internet is working again then 🙂 (I have seen your Tweet on your internet provider…) Since you mention that you’re inclined to go with marker cap weightings as far as stocks are concerned, and so have as much as 50% in the US, I imagine you don’t think it’s worth to listen to 10 yr forecasts? Vanguard’s are:

Domestic 3%-4%

international 6%-7%

And companies like RA and GMO also have higher forecasts for international. Would this not suggest that underweighting the US might perhaps be a good idea?

Yes, the internet is back — 36 hours later. No surprise here: It’s hard to run a website when you can’t access the web! I’ve seen the forecasts and the betting man in me is inclined to agree. But at 50% foreign stocks, I already have far more in foreign stocks than most U.S. investors. Anything more would represent a market bet that I couldn’t, on theoretical grounds, justify.

The best reason to be invested in ex-US stocks right now:

Thanks for sharing. That’s a frightening chart.

With a different X axis scale the legend might also read: “probability patience of value investors is tested” 🙂 I love reading financial history because it keeps me grounded through times like this. “Triumph of the Optimists” by Dimson/Marsh/Staunton is a favorite despite its textbook-like pricing. Another (more painful) read is “The Great Depression, A Diary” by Benjamin Roth. Reminds me of the value of cash/gov’t bonds in the portfolio when ‘blood runs in the streets’, as Bernstein wrote.

I would very much like to see a study that compares performance of the world excluding the US vs. the US (low-cost, index funds) that removes the fluctuation caused by the exchange rate. I believe (and yes, I know the difference between “believing” and valid scientific evidence – that’s why I’d like to see this) that the market rewards you for taking risks, but that it does not reward you for unnecessary risk. The exchange rate seems to me (am I wrong?) like a zero-sum game that just adds noise and is therefore, an unnecessary risk. And it seems to me that when non-US markets outperform US-only markets, it’s because of the exchange rate.

Does such a study exist?

I also “believe” that over the long-run, holding bonds hurts performance. There are thousands of articles, especially after a large market downturn, showing how much less one would have lost if they’d just had x% of their money in bonds, but they ignore how much growth you give up during the good times. I don’t “believe” (not sure if quotes apply here – this seems to be a fact) that one cannot time the market, so being in stocks during the uptimes, and diluting with bonds in the downtimes can only be done in retrospect.

Until I’m less than a decade (perhaps as little as 3-5 years) from retirement, it seems like I’m better off in a US stock index fund. For that reason, I’m 100% VTI (Vanguard total US stock market ETF).

If you want to look at various market indexes both in local currencies and in dollars, try:

https://www.msci.com/end-of-day-data-search

Click through to the regional indexes, click on one index and then you have the ability to see returns for that index in both local currencies and in dollars. Even if you look at returns in local currencies, I think you’ll find that there are often significant year-to-year and decade-to-decade differences in returns between U.S. and foreign stocks.

You’re correct that currencies are a zero-sum game on a worldwide basis. But the risk is real. Indeed, you can put a price on eliminating it — through hedging, which can either cost you money or make you money, depending in large part on short-term interest rate differentials.

Stocks should indeed outperform bonds, because they’re riskier — and it’s a risk you can’t diversify way. But are we talking expected returns. If those returns were guaranteed to be better, it wouldn’t really be risk. Thus, the reason we own bonds is because stock-market risk may not be rewarded, not only in the short-term, but also over extended periods. Again, I reference my favorite example: Japan. For three decades, investors in Japanese stocks have taken stock-market risk — and not been rewarded.