FREE NEWSLETTER

SECTION 415(D) OF the IRC requires the Secretary of the Treasury (IRS) to annually adjust limitations for cost-of-living increases. So, let’s dive into some of the changes:

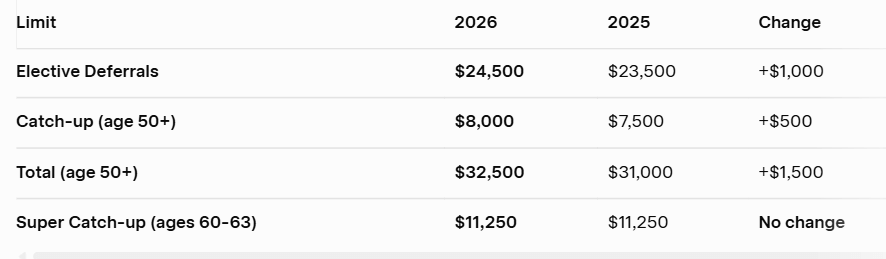

401(k), 403(b), and Most 457 Plans:

For 2026, the 401(k)/403(b)/457(b) amount you can contribute is increasing from $23,500 to $24,500. If you are in a 24% marginal tax rate, that’s an additional $240 of federal taxes you can defer. If you are over age 50, the catch-up contributions are also increasing by $500, which is a small increase.

Defined Contribution Plans, §415(c)

The annual total contribution limit is increasing to $72,000 (up from $70,000).

This means that your employee contributions + employer contributions + after-tax contributions cannot exceed $72,000 in 2026.

Many people only have employee + employer contributions, but if you are self-employed with a Solo 401(k) or working for a big Fortune 500 tech company, you may have the option of making after-tax contributions. The strategy is called the “Mega Backdoor Roth,” which allows you to contribute thousands extra into your Roth 401(k)/Roth IRA.

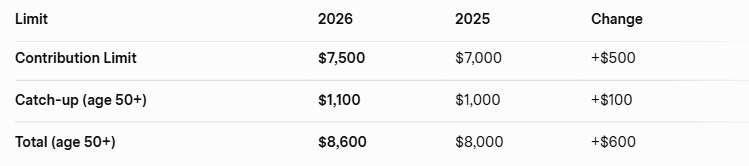

IRAs (Traditional & Roth)

For 2026, the Roth/Traditional IRA limits are increasing by $500 to $7,500.

Note that the Roth IRA income limits to contribute are also increasing in 2026. Direct Roth IRA contributions aren’t allowed if your modified adjusted gross income is over $168,000 (single) or $252,000 (married filing jointly).

However, you can still use the “Backdoor Roth” strategy to get around these income limits by doing a non-deductible IRA contribution that gets converted into a Roth. Just make sure you are aware of the pro-rata rule.

Other Adjustments

Earlier in the month, IRS released more details on other key adjustments for 2026:

1. Standard deduction

Married filing jointly: $32,200 (from $31,500)

Single: $16,100 (from $15,750)

Heads of households: $24,150

Note that the OBBBA also increased the standard deduction from $15,000 to $15,750 for 2025.

2. Estate tax exclusion

The estate tax exclusion is increasing from $13,990,000 in 2025 to $15,000,000 in 2026 due to OBBBA changes.

3. HSA

In 2026, you can contribute up to $4,400 if you are covered by a high-deductible health plan just for yourself, or $8,750 if you have coverage for your family to HSA.

4. Tax Brackets

All tax bracket limits are increasing by ~4%. Here are the 2026 brackets:

5. QCD

The QCD limit (age 70½+) is also increasing to $111,000 (from $108,000), which is the maximum charitable gift from an IRA that can be excluded from your income.

So overall, most of the deductions or limits are increasing by 3–4% on average.

Take advantage of these limits and maximize your tax-efficient retirement savings!

![]() Bogdan Sheremeta is a licensed CPA based in Illinois with experience at Deloitte and a Fortune 200 multinational.

Bogdan Sheremeta is a licensed CPA based in Illinois with experience at Deloitte and a Fortune 200 multinational.

Additionally, there is an Enhanced Deduction for Seniors from the OBB for individuals 65 and over. Through 2025-2028, singles can claim an additional $6000, married $12,000 (both 65+) annual deduction. The thinking was this deduction would more than offset taxes from taking Social Security. Plus, this deduction will be adjusted for inflation.

Very helpful. Regarding HSA, individuals 55 or older can contribute an additional $1,000 catch-up.

Do you know why a QCD to a donor advised fund is not allowed? Or, whether there is any plan to change this rule?

Thank you for this info and your weekly in-depth articles on advanced topics!