FREE NEWSLETTER

WELCOME TO OUR inaugural monthly personal-finance update. I was all ready to write about January’s robust stock market—and then the GameStop saga garnered national headlines, with short-selling hedge funds losing billions, everyday investors crowing and politicians piping up. Some bashed Wall Street for allegedly thwarting retail traders, while others worried about the financial system’s stability.

Amid the tumult, the S&P 500 fell into the red for the year-to-date, despite blockbuster earnings reports from two of the market’s longtime leaders, Microsoft and Apple. Renewed concerns about the economic impact of COVID-19 also weighed on the market.

Still, small-company stocks’ gains weren’t entirely erased—further proof for the so-called January Effect, the tendency for small stocks to outperform during the year’s first month. Vanguard Small-Cap ETF (symbol: VB) held on for a 2% gain, despite losing nearly 5% in the month’s final week. But the S&P 500 closed the month down 1%. Does that put the kibosh on 2021? The January Barometer, sometimes confused with the January Effect, posits that as goes January, so goes the year. But such Wall Street lore is more proverbial than tradeable.

Should auld acquaintance be forgot? Large-cap U.S. growth stocks, seemingly so unbeatable for so long, reached peak outperformance in early September. As a group, the stocks continued to lag behind small caps in January, with Vanguard Growth ETF (VUG) down 1%. Tesla (TSLA), up 12% last month, was the biggest exception, though Microsoft and Google’s parent Alphabet gained 4% and nearly 5%, respectively. Vanguard Small-Cap Growth ETF (VBK) and Vanguard Small-Cap Value ETF (VBR) both gained some 2%, as their investment styles sparkled, as they have for the past three months, with advances of 26% and 28%, respectively.

Truth be told, the Vanguard Extended Market ETF (VFX), which tracks small- and mid-cap stocks, bested both of them over one month (+3%) and three months (+30%). The latter result was powered by former index component Tesla, which is up nearly 600% over the past year and is now the nation’s fifth-largest company by stock market capitalization. The electric car maker was added to the S&P 500 index on Dec. 21 and is no longer held in Vanguard Extended Market.

Asia ascendant. Some of the best action around the globe in January was along the Pacific Rim. BlackRock’s iShares MSCI China ETF (MCHI) gained 8% and iShares MSCI Taiwan ETF (EWT) was up 4%, despite significant declines in the final week. That drove broader emerging markets funds higher, with Vanguard FTSE Emerging Markets ETF (VWO) climbing 3%.

Based on reported data, China was the only major economy to grow in 2020, apparently helped by aggressive containment of COVID-19. Foreign stocks as a whole slightly outperformed the S&P 500 in January, as reflected in a 0.4% gain for Vanguard FTSE All-World ex-U.S. ETF (VEU). But foreign small-caps didn’t get the memo that it was time to shine, with Vanguard FTSE All-World ex-U.S. Small-Cap ETF (VSS) down 0.6% last month.

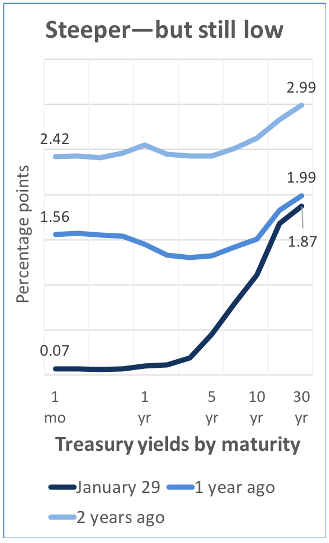

Steeper curve. In recent memory, the yield curve—the relationship of longer-term Treasury bond yields to those of shorter-term Treasury yields—has been somewhat flat. No more. The Federal Reserve has pushed short-term rates to the floor, while optimism about a recovery has pulled long-term yields higher. Whereas the short and intermediate areas of the curve used to offer an attractive mix of income and safety, yields there are now low both in absolute terms and relative to longer-term yields.

Steeper curve. In recent memory, the yield curve—the relationship of longer-term Treasury bond yields to those of shorter-term Treasury yields—has been somewhat flat. No more. The Federal Reserve has pushed short-term rates to the floor, while optimism about a recovery has pulled long-term yields higher. Whereas the short and intermediate areas of the curve used to offer an attractive mix of income and safety, yields there are now low both in absolute terms and relative to longer-term yields.

The yield advantage of 10-year Treasurys over two-year Treasurys recently hit its highest level since mid-2017. But before you don your climbing gear, realize that even the 30-year yield, which ended January at 1.87%, is far lower than it was two years ago, when the long bond yielded 2.99%. That’s a lot of room for rates to rise and hence for investors to lose a ton of money in a long-term Treasury fund.

For instance, the Vanguard Long-Term Treasury ETF (VGLT) has an average duration—a measure of interest-rate sensitivity—of 18.6 years. That suggests that if long-term rates were to rise one percentage point—say, back to 2019 levels—the fund’s price would fall more than 18%. (On the other hand, it would gain that much if interest rates fell one percentage point.) The Vanguard fund slumped 3.5% in January, but still has a gain of nearly 6% for the past 12 months. Perhaps online savings accounts, yielding in the half-percentage-point range, are better places today to park your safe money.

William Ehart is a journalist in the Washington, D.C., area. In his spare time, he enjoys writing for beginning and intermediate investors on why they should invest and how simple it can be, despite all the financial noise. Follow Bill on Twitter @BillEhart and check out his earlier articles.

William Ehart is a journalist in the Washington, D.C., area. In his spare time, he enjoys writing for beginning and intermediate investors on why they should invest and how simple it can be, despite all the financial noise. Follow Bill on Twitter @BillEhart and check out his earlier articles.

Want to receive our weekly newsletter? Sign up now. How about our daily alert about the site's latest posts? Join the list.

I struggle to understand the way bond funds work vis a vis the yield . Can someone explain it like I am retarded because based on my WSB membership I am

If interest rates rise, bond fund yields should also rise, but their share price will fall. To find out how much, find out a fund’s duration:

https://humbledollar.com/money-guide/risk-and-bond-returns/